Yes the Fed is very likely to cut rates very aggressively over next 12 months but this only likely to start after payrolls ( charts 14, 15) turn negative

Next he feels in this week’s Flow-Show report that this will all end (after the next coming rate cuts) in a bearish tipping point for the US dollar.

His reasons are plenty:

investor worries over lack of policy coordination between Fed-UST to ban bank runs,

new political targeting of the Fed,

profound foreign worries over US debt ceiling,

CBO forecasts of >5% US deficits next 6 years,

non-stop spending on war…

These ongoing stressors on the dollar will not take kindly to the next easing cycle. That “Dollar tipping-point” will start a bear market cascade in which the dollar will be dropping while stocks under-perform (more on that in a minute). It will also force bond yields higher ( inflation will migrate out on the curve as Zoltan said before), and may ultimately need Fed YCC or QE to constrain upside for yields.

Hartnett's punchline is also his "endgame" trade recommendation - go all in the next big recession, when the Fed goes all-in "Japan", and is forced to launch yield curve control (YCC) the same way it did during World War 2, to keep the dollar reserve status

Sell Stocks As Rates Top

But now he is getting even more specific. He’s actually saying that despite the coming rate easing to sell stocks at the last hike, not buy them.

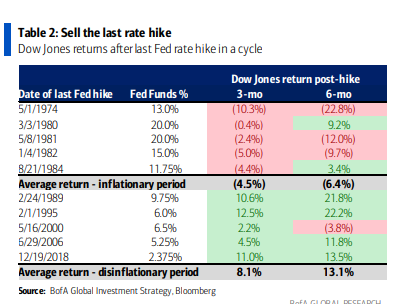

'Sell the last hike' was the correct strategy for stocks in inflationary '70s/'80s rather than 'buy the last hike' which worked in the more recent disinflationary market of '90s+…

This is a quite brilliant take (to us anyway) because he thought to use the Inflation-as-Tailwind concept Pozsar had brought up months ago, but Hartnett applied it in a more practical fashion.

Prices were a steady source of disinflation for the past two decades, which gave the Fed precious time and cover to figure out what to do with policy rates to control services inflation. Not today. Goods inflation is now a tailwind.

We are in those inflationary tailwind times Pozsar describes. Therefore, Hartnett grouped stock moves post a final rate hike to by inflationary vs disinflationary eras. Here is what he found:

Stocks fell in the 3 months after every last hike in the '70s/'80s (Table 2)…

We think that happens in 2023 as negative feedback loop from higher unemployment to day traders, retail, consumers, corporations likely very pronounced…

He then thinks stocks are a buy1, but that timing is less quantified.

[T]hat’s the final lurch lower we want to buy, and it’s secular leadership of inflationary cyclicals we will buy, not old leadership of credit, PE, large cap tech.