HouseKeeping: Thank you for reading our work. This Report is meant to be read like Barrons Weekend or Sunday papers were back in the day. Some data, some market concepts, some history. Enjoy

For the holidays all subscribers can get 20% off annual memberships. Prices will likely go up in first quarter next year.

SECTIONS

Market Summary: weekly recap

Precious: analysis

Reports: research

Technicals: active trading levels

Podcasts: GoldFix and Bitcoin

Charts: related markets

Calendar: next week

1. Market Summary

Call it a reality check that things can not be this distorted for this long without serious consequences if/when things go the other way.

This week saw the S&P rip to its best week since February as Goldman's melt-up appears to have come true. Friday was dominated by CPI - which printed at its hottest in 40 years but was modestly below the whisper number - and that sent yields lower (especially the short-end) and implicitly Nasdaq and S&P (growth) higher as Small Caps (value) lower. Everything went vertical in the last couple of minutes.1

Morgan Stanley had this to say on Friday after CPI

Despite alarming inflation headlines, financial markets seemed to be relieved at Friday's CPI numbers. For the first time in months the month-over-month increase of 0.5% was in line with expectations instead of delivering an upside surprise.

They went further to add they saw material changes in pipeline congestion which indicated easing of inflation pressures due to supply chain issues.

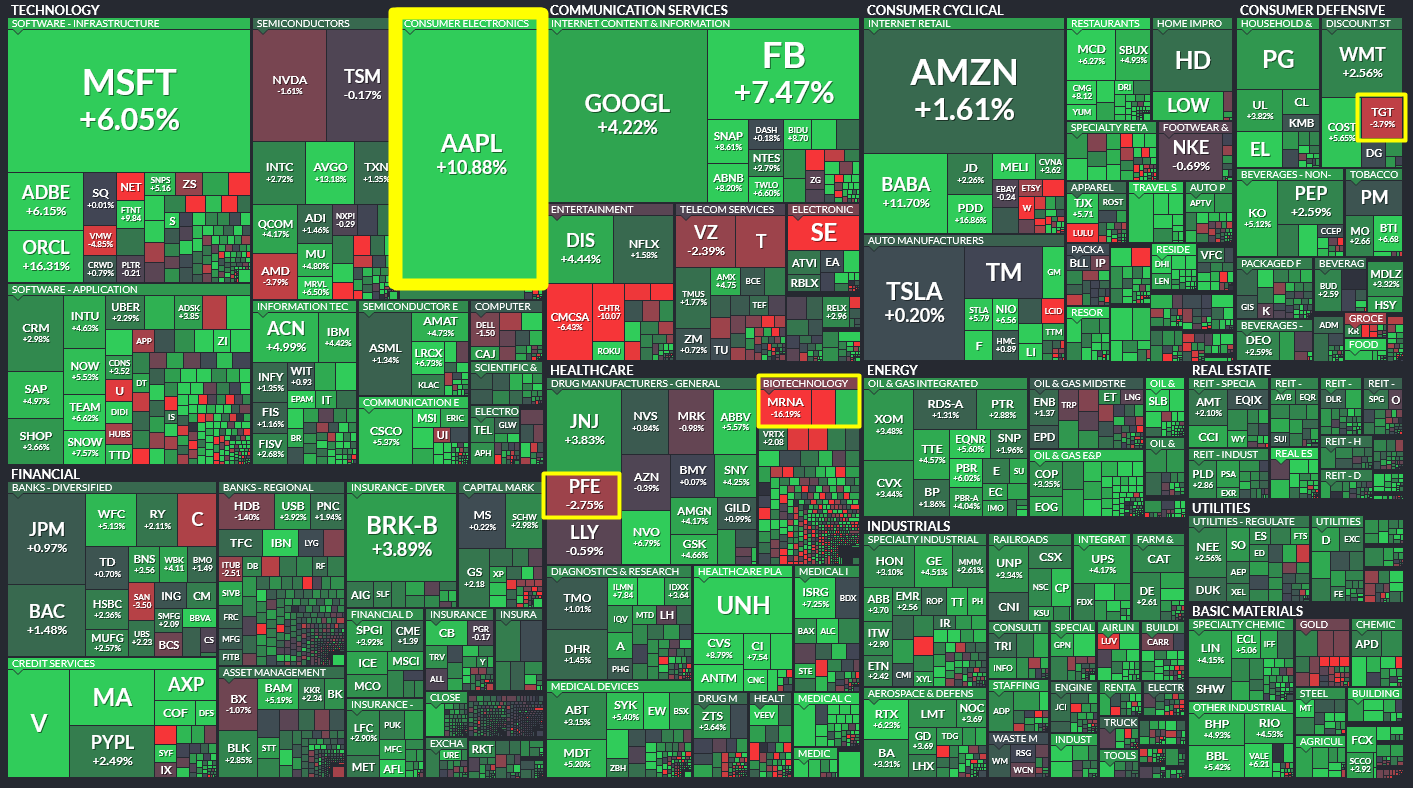

A record close for the S&P 500

This week's gains in stocks were ignited by a major short-squeeze in the first half of the week, but that faded as the week wore on.

Sector Performance:

Unprofitable tech stocks rallied for the first weekly gain in a month and biggest weekly gain since early October

AAPL appears destined for $3 trillion market cap, having been positive both weeks

Last Week Omicron Sea of Red

This Week Fields of Green

Amid all the excitement, Defensives actually outperformed Cyclicals on the week.

Tesla languished on Musk’s new hair do perhaps

Moderna took a major hit on its Flu vaccine test being placebo-like

Bonds:

It is worth mentioning that the yield curve is still discounting a price hike in 2022 as a policy error. Essentially the curve is implying that the fed will hike; and in doing so it will be hiking into a slowing/ stagflationary economy. That could all change in a heartbeat, but it is worth noting this has been moving in that direction for almost a month.

So forgive us for obsessing but things like this frequently resolve in a violent bond curve adjustment followed by a major stock move. The implications aren’t necessarily bearish for stocks, but they are predicting some more volatility.

The whole thing could resolve with