BBG: Entering the Real Rate Sweet-Spot

Real yields should provide an even greater tailwind for gold through the rest of 2023, supported by a weaker dollar and by buying from reserve managers.

Gold Tailwinds Rising As It Enters Real-Yield Sweet Spot

By Simon White, Bloomberg Markets Live reporter and strategist courtesy ZeroHedge

Real yields should provide an even greater tailwind for gold through the rest of 2023, supported by a weaker dollar and by buying from reserve managers.

Gold is flirting with all-time highs versus the dollar and several other currencies, while it is at its highs versus several more currencies, such as the Japanese yen, the Australian Dollar and the Indian rupee.

Gold is often simplistically taken as an inflation hedge. However, the correlation between gold returns and CPI is very close to zero over the long term. Instead, the interplay between inflation and interest rates — i.e. real rates — is more meaningful for gold.

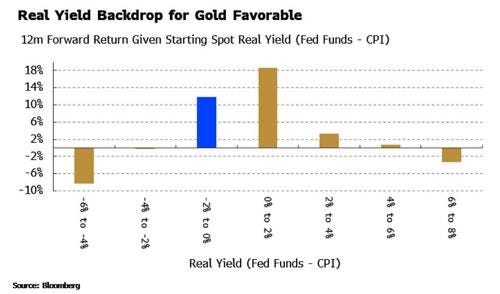

Gibson’s Paradox stemmed from the observation that real interest rates and gold move inversely to one another (named a paradox by Keynes as it contravened standard economic theory). Gibson’s Rule said that for every percentage point the real fed funds rate was below 2%, gold should rally 8% over the next year.

The data gives a more nuanced answer. The chart below shows the subsequent one-year return of gold (in dollars) for different real-rates buckets. There is more of a parabolic relationship with real rates and gold rather than a straight line.

Real rates (-1% now) are currently very favorable for gold on historical basis.

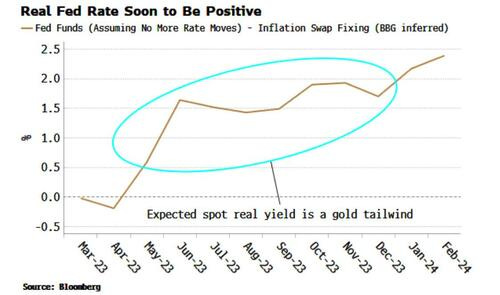

Furthermore, real rates are set to get even more gold-friendly. CPI fixing swaps and the current level of Fed rates show that the spot real rate is expected to be between 1% and 2% for most of the rest of this year, i.e. in the most favorable bucket for forward gold returns.

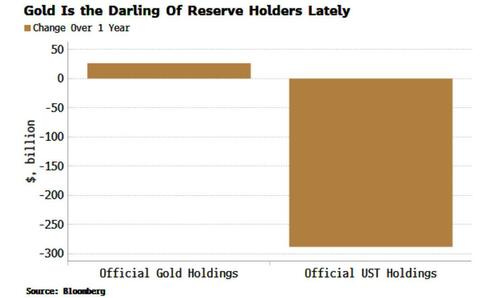

If we add to this real buying from reserve managers, the backdrop has fundamental support. It is way too premature to call the end of the dollar as the world’s reserve currency, but it is clear countries are diversifying away from USTs, and some of the gap is being filled by gold.

Add in a dollar downtrend that looks intact for now, and gold should continue to perform well, and quite conceivably start making all-time highs in several more currencies, not least the dollar.