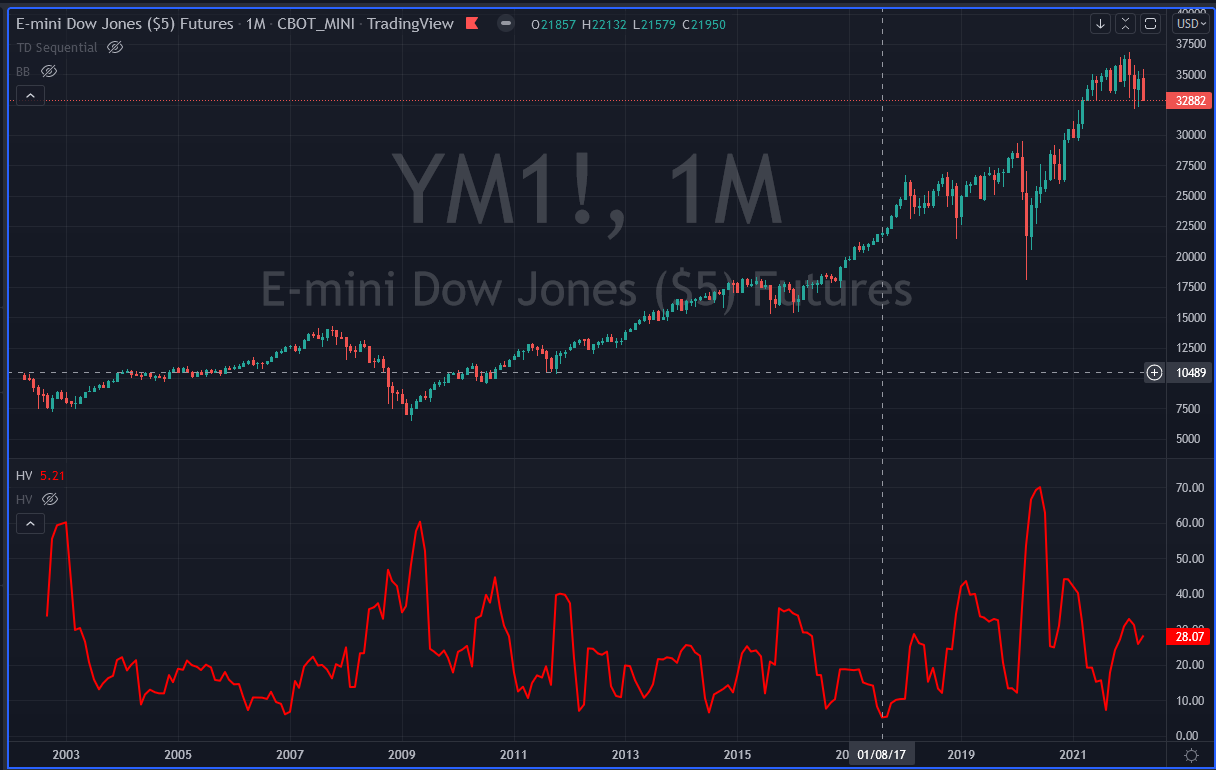

One of the best available and accepted tools to measure stock market volatility is CBOE Volatility Index, elaborated by Chicago Board Options Exchange in 1993.[11] In other words, VIX can be defined as a sentiment ratio of Wall Street's fear or greed gauge. It is usually used by traders to check the grade of investor complacency or market fear.[12]

In practice, VIX is usually called the fear index. In case of increased VIX index, investors' sentiment leans toward higher volatility which corresponds to higher risk.[13] If a VIX reading is under 20 it usually indicates that investors became less concerned;[11] however, if the reading exceeds 30 it implies that investors are more fearful because prices of the options increased and investors are more prone to pay more to preserve their assets.

- Wikipedia

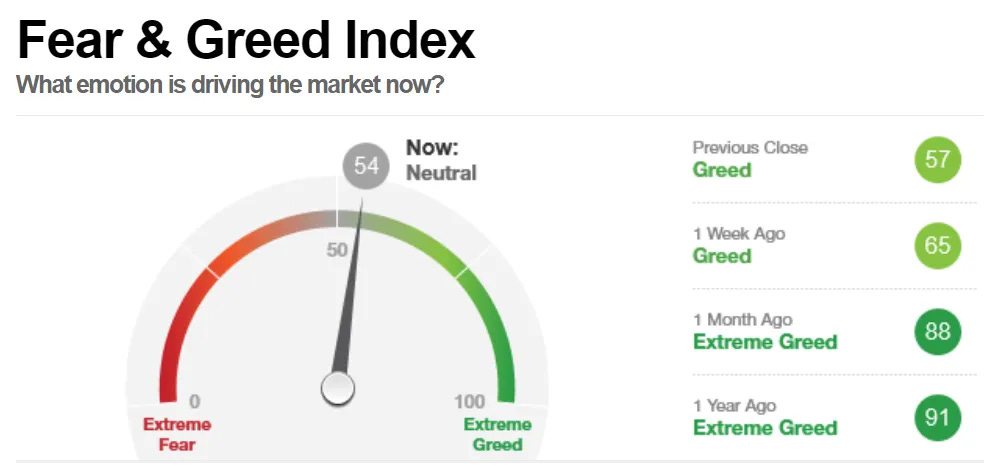

Fear and Greed in stocks is indicative of dominance.

WORK SHEET: IDENTIFYING FEAR and GREED LEVELS

Stocks

Metals:

Energy

What is volatility

implied

Realized/ historical

1987 crash:

indexing, portfolio insurance, the crowded trade of ‘martingale-method’

Hedging long stock risk post 1987

Buy insurance

Create dividends, lower cost basis

Collars are invented

The effect on Option markets-

Calls sold, Puts bought

Stock Market “tell” is born

Why Vol expands in a dropping market and drops in a rally

Who is long stocks, who is short stocks

Stochastic volatility- who is most likely to panic first

The Vixx created 1993: The rise of Volatility as a reliable predictive indicator

2004- Vixx Futures listed : the arbitrage begins

Introduced in 2004 on Cboe Futures Exchange℠ (CFE®), VIX futures provide market participants with the ability to trade a liquid volatility product based on the VIX Index methodology.

GFC and 2009: death of predictability:

In January 2009, S&P Dow Jones Indices launched the S&P 500 VIX Futures Index Series

the Fed (PPT) sells volatility,

the tail wags the dog.

Rise of Vixx by TV Popularity

Misuse by TV

the rise of over bt/oversold contrarian use

Implied vs Realized as indicator

The rise of skew as modifier

What you can absolutely know by Vol/skew indicators

Risk/reward

dominant player types- buyers and sellers

advanced use- stochastic vol plays

The world since 2009- stock buybacks, short squeezes, and dark pools

Gold options pre GLD and post GLD as example

who dominated

Why did they dominate

Skew as tell

VBS

Option modeling example graphs

Notional Area

Smile

“law” of conservation of volatility: Vol, skew, kurtosis knobs

skew in notional

skew in smile

ATM vol predictability given a move in mkt

Fat tails: Kurtosis-

Option Work sheet

Old man story:

Options Education: Lehman brothers executives and Rule 144, client buys calls, getting hired at CNA, Roy Neff at christmas party, PDE model guinea pig, life experience, Pit Trader, CSO modelling, from commodities to equities to commodities, AMEX- Timber hill/ CRT, Susquehanna. Gold, and manipulation