Founders: Understanding Option Volatility

Good Morning. Attached is an early intermediate-level video along with some notes on volatility that were previously used for university coursework. The material is far from perfect, but it reflects the type of structure that was requested and should provide a useful starting point for discussion. The link is included below.

The notes come from a separate lecture on “time value,” which at its core is closely tied to volatility.

Today’s Founders class will focus on CFTC COT coverage, along with any questions you may have on this material.

LECTURE NOTES

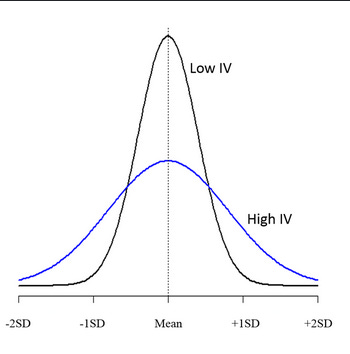

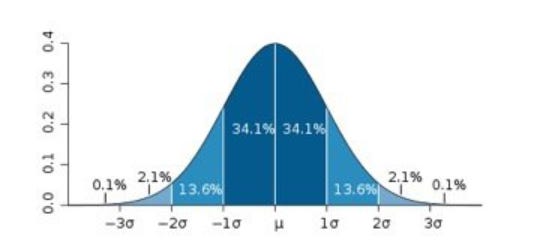

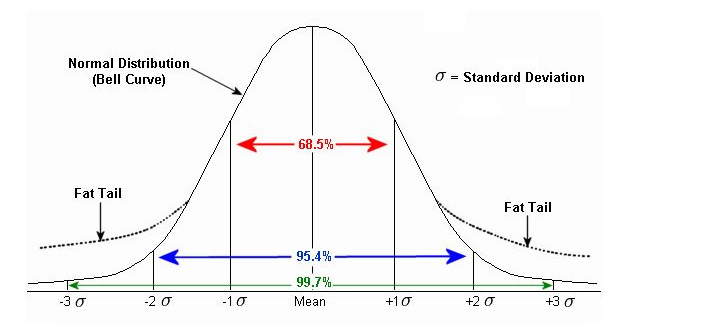

VOLATILITY VISUAL AIDES

Dark Blue= 1 Vol or 1 STD

Dark Blue plus light blue= 2 Vol or 2 STD

A market with stable Vol remains within a range of movement 68.5% (1 Vol or STD) of the time and 2 Vols 95.4% of the time etc.

Low Vol spends more (more data points) of its time closer to the mean

Higher vol has a a bigger distribution around the mean