Gold Price Forecast “Constructive” Despite Headwinds: Where Gold Prices Are Headed in 2026

Devere Group

The outlook for gold prices remains “constructive” despite the headwinds posed by the war in Iran.

Gold prices slumped following the outbreak of the conflict and remain well below pre-war levels, when the yellow metal traded over $5,000 per troy ounce.

But strategists say gold could be poised to bounce back before year-end, and could reclaim the $5,000 level.

That’s according to Ewa Manthey, commodities strategist at ING, who said that the long-term structural supports for the gold rally remain in place.

While the near-term risks are yet to subside, the long-term case is clear, according to Manthey, who believes there could be around six per cent upside in the coming months.

In a May 11 report seen by deVere Insights, Manthey said the inflationary blowback from the Iran war had put the brakes on the gold rally, but that the bull case is underpinned by “structural pillars.”

Those pillars include resilient demand from central banks, which are engaged in a gold-buying spree.

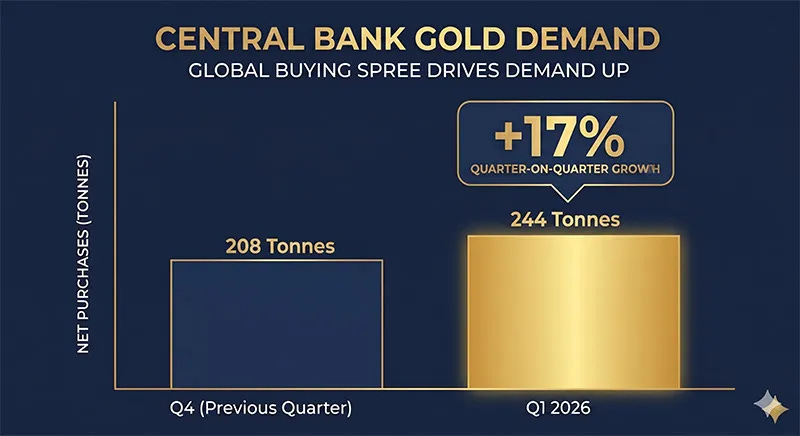

Despite an increase in gold sales, particularly on the part of Turkey, overall central bank demand for gold grew 17 per cent in Q1.

The People’s Bank of China is also continuing to accumulate, adding eight tonnes of gold in April alone, demonstrating that reserve diversification is “remaining supportive for gold over the medium term.”

At the same time, momentum is rebuilding behind gold ETFs, which saw large outflows after news of the war sparked a liquidity squeeze.

The latest data shows ETF flows turned positive in April, following net outflows in March, signalling renewed investor interest.

Manthey said the coming months may be shaped by the outcome of peace negotiations, with risk tilted toward the downside should they fail to make headway.

But, once the war comes to a conclusion, “gold’s underlying support should reassert itself.”

It’s a widely shared view amongst metals analysts, who continue to argue that the gold rally has road to run. They see the Iran war as a hurdle, rather than a roadblock, which has slowed, rather than stalled, the rally.

A recent Reuters poll of 31 metals analysts found a consensus view that the gold rally would resume once the Iran war was brought to an end, with a median forecast of $4,916 in 2026.

Responding to the survey, independent analyst Ross Norman said that far from derailing the rally, the Iran war had bolstered the fundamentals:

“The motivation for central banks to acquire gold is arguably stronger than ever , and events in the Middle East will only have amplified? a sense of vulnerability to dollar assets. In short, gold looks positive but in a more measured way.”

Will Gold Prices Go Up? Analysts Bullish Despite Near-Term Risks

Analysts are converging around a clear narrative: the Iran war has been a setback for gold, but there should be upside for the yellow metal before year-end, and the potential for further gains in the coming years.

That’s in large part because the gold rally, which has seen prices rise by more than 160 per cent in five years, is seen as a response to structural macroeconomic and geopolitical changes.

Russia’s invasion of Ukraine was the final nail in the coffin for the “end of history” thesis. Fresh off the heels of a pandemic, we were forced to face up to the fact that the 80 years of relative peace and stability since the end of World War II were an anomaly, rather than the new normal.

That war, which remains ongoing, was followed by major conflicts in the Middle East, with the fallout cascading across the globe. Old assumptions about free markets, freedom of navigation, and multilateral cooperation have been ripped up.

The world now looks more unpredictable than ever. We are seeing major rearmament both in the West and in the East. There is a clear shift away from the dollar as the world’s reserve currency, and a scramble to secure strategic resources.

It’s in this context that gold, a store of value for thousands of years, comes into its own. The threat of war, currency debasement and an uncertain outlook place a premium on gold as a port in the storm.

Some market observers note that gold’s status as a safe-haven failed to assert itself during the Iran war, with the yellow metal falling, rather than rising, in response to the conflict. But that’s because of the particular characteristics of the conflict, which have weighed on precious metals.

One of the primary impacts of the Iran war was to send energy prices spiralling. The petrodollar system means higher oil prices put upward pressure on demand for US dollars, increasing the value of the greenback.

When the value of the US dollar goes up, we often see the price of gold fall, because it is priced in dollars, making it more expensive for foreign buyers.

What’s more, the expected inflationary pass through from the energy price spiral has derailed a favourable rate cut outlook this year, with traders no longer pricing in a Fed cut in 2026.

Gold tends to do best in an environment with low interest rates and a weak dollar, going some way to explaining why it has performed poorly since the outbreak of hostilities in the Gulf.

However, the conflict and its impact look temporary, rather than structural. Sovereign debt continues to pile up, industrial powers like the US are keen to keep a lid on their currencies in order to maintain an efficient export market, and the growth in the M2 money supply shows no sign of stopping.

In other words, the Iran war has been negative for gold prices, and there remains an enormous uncertainty in the outlook around the outcome of ongoing peace talks. A breakdown in the talks and a resumption of hostilities is a clear downside risk in the short-term.

But beyond the conflict, analysts remain bullish for gold over a longer time horizon, because the environment now looks very favourable for precious metals. Currency debasement, de-dollarisation, and instability now look like structural realities, not temporary blips.

Where Are Gold Prices Headed in 2026?

In broad terms, the near-term outlook remains uncertain and fraught with volatility, while the long-term outlook remains constructive to bullish.

Many year-end price targets will have been derailed by the Iran war, with Saxo Bank’s Ole Hansen telling deVere Insights his $6,000 call may now be pushed back by six months.

With peace talks ongoing and the ceasefire between the US and Iran looking increasingly fragile, there is a great deal of uncertainty as to where gold will be by the end of 2026, not least because of the importance of oil prices to the outlook.

As such, we see a significant range between forecasts, with bullish predictions putting gold at $5,000 per troy ounce before the end of the year, some suggesting gold will continue to trade sideways, and others calling for gold prices to fall in the coming months.

In recent weeks, analysts have warned of downside risks to the gold price being thrown up by the peace talks, which have so far failed to produce results satisfactory to any of the parties to the conflict.

Analysts at Goldman Sachs have warned that their near-term gold outlook is skewed to the downside because of risks to transit through the Strait of Hormuz.

However, the bank’s medium-term outlook remains tilted to the upside because geopolitical developments could “accelerate diversification into gold and to weigh on perceptions of Western fiscal sustainability,” according to a note penned by Lina Thomas and Daan Struyven.

Gold Price Outlook 2026: Why the Bull Case Still Holds Despite the Iran War

For now, the gold price outlook remains caught between two opposing forces. On one side is the immediate pressure from the Iran war, inflation, a stronger dollar, and a less favourable interest-rate backdrop.

On the other hand, there is the deeper, more durable case for gold, which revolves around central bank accumulation, de-dollarisation, fiscal stress, geopolitical fragmentation and the growing appeal of hard assets in an increasingly unstable world.

That tension helps to explain why gold has failed to behave like a classic safe-haven asset during the latest phase of the crisis.

Instead of pushing investors straight into bullion, the energy shock has strengthened the dollar and clouded the rate outlook, both of which have weighed on prices in the short term.

But the long-term outlook remains constructive. Central bank demand remains elevated, despite some selling in March, with the World Gold Council reporting 244 tonnes of net purchases in Q1 2026, up 17 per cent quarter-on-quarter.

Gold-backed ETFs also returned to inflows in April, adding $6.6bn and lifting holdings by 45 tonnes, suggesting that institutional investors are again rebuilding exposure after the March sell-off.

A breakdown in peace talks, further disruption to the Strait of Hormuz or another surge in energy prices could keep gold volatile in the near term. But if the conflict eases, the structural supports that drove the rally in the first place are likely to reassert themselves. As a result, gold looks likely to reclaim the $5,000 level – if not this year, then next, as the key catalysts, currency debasement, instability and central bank demand reenergise the rally once the current crisis wanes.

Peace vs Gold:

Who needs flood insurance in a drought.... and then the rains came.

"constructive"--no one's going to lose their job with that powerfully non-committal descriptor.