Gold's Role Evolves From Haven Asset to Functional Reserve Instrument

GFN – LONDON:

Central banks, which have accumulated gold reserves at historically elevated rates over the past four years, are increasingly weighing asset liquidations to fund rising energy and defense expenditures, a shift that analysts say could rebalance gold’s role from speculative instrument to functional reserve asset.

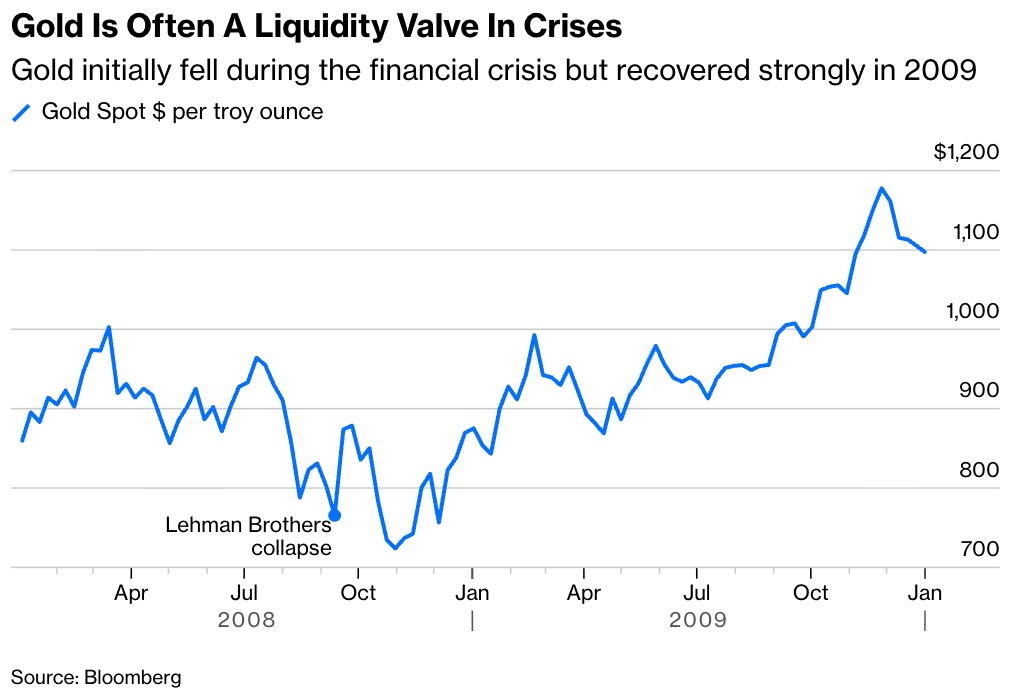

Gold prices have declined approximately 15% since the escalation of the Iran conflict, a correction that market participants have compared to similar liquidity-driven selloffs during the 2008 global financial crisis and the initial onset of the Covid-19 pandemic in March 2020, according to industry analysts (via BBG).

Despite the pullback, the metal remains up more than 50% over the past twelve months and more than 150% over five years, leaving many institutional holders with substantial unrealized gains. The World Gold Council, an industry body, estimates that central banks collectively hold more than $4.3 trillion in gold reserves, representing approximately one-fifth of the market, roughly double their long-term historical share.

“Central banks bought just five net metric tons of gold in January, versus a monthly average of 27 tons last year,” the World Gold Council said.

The accumulation trend accelerated following Russia’s 2022 invasion of Ukraine, with China leading diversification away from dollar-denominated assets after the United States Treasury’s Office of Foreign Assets Control coordinated the freezing of approximately $330 billion in Russian sovereign reserves, according to the Brookings Institution. Russia has since become the largest gold seller of the current year, a development the World Gold Council attributes in part to efforts to stabilize the ruble. The governor of the National Bank of Poland, the largest single buyer in the prior year according to the World Gold Council, recently raised the possibility of liquidating a portion of its holdings in discussions with the Polish president.

Separately, Bloomberg News reported that Turkey’s central bank is considering using gold held at the Bank of England as collateral to support the lira rather than pursuing direct currency market intervention. Industry publication mining.com has identified several major Middle Eastern and Asian central banks as additional potential sellers.

The emerging pattern suggests gold is transitioning from a period of concentrated accumulation into a more balanced market structure, with reserve management considerations rather than speculative demand increasingly driving institutional activity.