Special CPI Prep | Market Rundown

JPM, Goldman, Barclays, MS and Trading Levels

Market Rundown:

Good Morning. The Dollar is down 6. Bonds are slightly stronger. Stocks are up another 65 bps on average. Gold is up $5. and Silver is up 12 cents. Crude is up 30 cents. Natural gas is up another 4%, 26 cents. Crypto is strong at up between 90 and 150 bps. Grains are all up some. Today is CPI

CPI CONSENSUS EXPECTATIONS

Headline YoY 7.3%, Core YoY 6.1%,

Headline MoM 0.3%, and Core MoM 0.3%. Overview

Coming into today’s CPI number Stocks have had a terrible December thus far, yesterday notwithstanding. If last month’s CPI was the most important for the Fed’s deciding to back off rate hikes, then this month will be the print that confirms if their decision to do so was the right one. Today’s number will heavily influence what the Fed has to say tomorrow in its press conference. But should not change their decision, whatever that decision is.

Last Month

November’s CPI came in significantly lower than expected at 7.7% when 7.9% was expected and stocks took off. The S&P rallied 5.5% and the Nasdaq ramped an incredible 7.5%

Historic CPI Returns…

A lookback at recent history shows that CPI day returns have been mostly ugly for stocks and mostly good for Gold. When CPI Beat expectations every month. That is, until November’s numbers. Which means: Stocks should rally on a lower number, and so should Gold.

How Important is This One?

Even though this report is largely expected to show continued moderation of inflation, the market may still have an oversized and protracted move even if the number comes in as expected.

Oversized because, well… look at what happened last month. If there is any money on the sidelines, (this is “buy season”) waiting for a catalyst to be deployed, all it needs is an excuse to enter the markets. End of Year deadlines for deployment are also approaching.

Protracted because there really isn’t much data coming out between now and mid January. So, whatever happens today may be the basis start of a month-long trend simply because of the fact that there are few important signposts between now and earnings season. ZeroHedge makes this point rather succinctly:

[T]he CPI print has the potential to dictate market direction and magnitude until earnings kick off in mid-January.

Bottom line, flows will dictate for the next month unless the Fed starts jawboning excessively.

There’s Always a “But”

On the other hand, if everyone is thinking like we are, then yesterday’s rallies may have been those same funds front-running that eventuality. Therefore, if the number comes in as expected or too hot, those types will puke first, then we can see if there is any dip buying from “all” the new allocations. Let’s quickly take in how players are looking at the CPI.

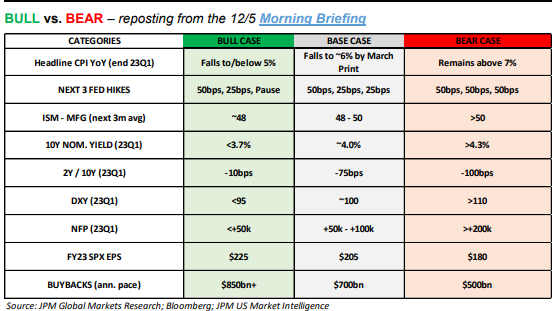

JPM’s CPI Cursory Matrix…

Dovish and Hawkish CPI Rationales

Doves will cite recent declines in commodity prices (Energy) and other data coming showing accelerating disinflation, e.g., used car prices are plummeting.

Hawks will focus on asset prices like homes which are still rising, and food, which is ramping higher almost continuously.

CPI Expectations and full analysis of Goldman, JPM, trading desks AND TECHNICAL LEVELS below…