Special Edit: The Big Rabbit Hole

Early Draft of The Big Long post with completely different idea flow

This is unfinished, unpolished and completely different path the thoughts took before posting The Big Long.

More conspiratorial, more accusatory, and more about the BRCS mindset. But not inaccurate.

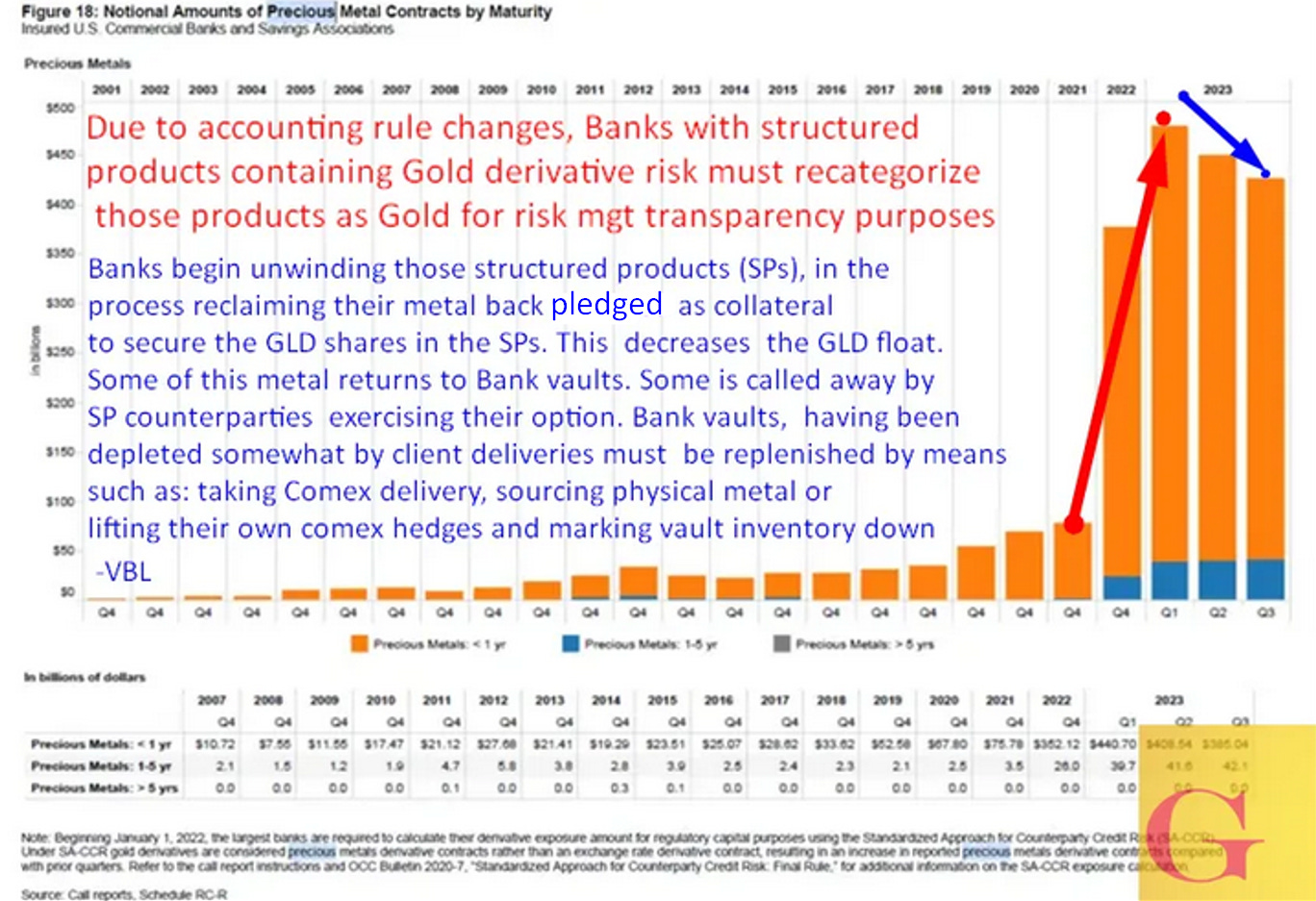

Remember when Bullion banks had to recategorize their Gold derivative risk as Gold from FX risk? This put JPM and CITI at over 90% of the Gold Derivative Marketshare while ballooning public totals by 500% from 79.28BB to $491.86BB overnight?

From our coverage in JPMorgan And Citi are 90% of The U.S. Gold Derivative Market

Starting January 1st, 2022, the largest banks became required to move all gold derivative risk, not currently in the “Precious Metals” risk category pictured above into that very category. Which Banks had the biggest changes? JPM, Citibank, and Goldman1 did. But JPM and Citi really stood out.

Some observed this as lies being uncovered, or in the very least obfuscation of risk. Though we can never know the intent of the original risk categorization, we can know the effect did in fact muddy risk analysis.

The next logical questions we thought back then were: “What made them do this now?” and “What changed?”

The reasons we assumed to be two-fold. The first one being: Basel 3 is forcing banks to disclose physical risk as Gold and Silver are delevered (and delivered) out of exchanges and onto more CB balance sheets.

The second reason was less accounting based, and more conspiratorial as the year unfolded

Later in the year JPM was made custodian of the GLD trust

Bloomberg: JPMorgan Joins HSBC as Vault Custodian for Top Gold ETF

JPMorgan Chase & Co. will store gold held by the world’s biggest exchange-traded fund in its vaults, a major coup for the bank’s bullion business. The lender will now act as an additional custodian for the SPDR Gold Trust- Bloomberg

Therefore it was assumed JPM had to put all its cards on the table as a requirement to get that powerful and potentially lucrative GLD custodianship deal.

They also had put that painful metals manipulation case behind them right before

Satisfied with that reason, we assumed Gold and Silver would rise in price SLOWLY due to this deleveraging and thus continued being structurally bullish and saying so here.

How much the metals would actually rise would be contingent upon skills the banks and government had in controlling shortside open interest closing down which if done sloppily, could drive prices higher faster as shorts were covered.

This controlled takedown of risk is something the Banks and government are quite skilled at executing when necessary, having witnessed it in many financialized markets in the past including (but not limited to) the paper Gold and Silver markets, oil multiple times, and LTCM etc.

The key to controlled takedowns in metals hinges on only one thing: That nobody withdraws their metal as collateral immediately.

That actually makes metals the easiest commodity market to control… because noone eats or consumes the Gold.. or frankly uses it as much as Bonds as an SOV at CBs ( bernanke called it “tradition” lol)

By delaying, or removing delivery of physical metal, paper contracts can work themselves out (expire or rollover) while banks continue to use the physical metal as collateral, sometimes even doing double duty via rehypothecation. That is a longstanding tenet of fractional reserve banking applied to metals.