Weekly: Gold and Silver Hypothesis Restated

Stocks are being manipulated non-stop now

Housekeeping: This Monday and every Monday we do a Silver/Gold podcast on Arcadia Economics. We request you take a look at our shows, and subscribe to the other excellent silver-based content on that site. Much of the content in our podcasts builds on comments we make here on metals. Sometimes it’s granular and actionable, sometimes more macro. This Monday’s broadcast will be on CTAs in Silver and ways the Fed may re-monetize Gold.

SECTIONS

Market Summary— Tiny Dog, Big Tail

Research— Alot

Week’s Analysis/Podcasts— CPI, Oil, Paulson

Charts—Silver, Gold, Energy, FX

Calendar— FOMC minutes, PCE

Technicals— GC, CL, BTC, SPX

Zen Moment— Birds and Bees

Full Analysis— Gold and Silver Manifesto

1. Market Summary

Recession still does not mean Fed Pivot. 'Good' macro news was 'bad' market news all week. Fed hawks spoke reaffirming as much. The result was the S&P was biggest loser on the week followed by The Dow. Small Caps outperformed.

The terminal rate popped above 5.3% seemingly on its way to 6%. Stocks continue to largely fight the fed, but are now giving ground. All the January buying is done. Financial conditions which had improved (new credit card pre-approved!) last month and gave good reason to be long stocks, have started to back off (sorry that credit card offer was cancelled!) again.

From Mester and Bullard to Williams and Barkin, every Fed Speaker was hawkish this week - 'higher for longer', 'more work to do', 'no rate cuts this year'... etc... and while the stock market tried to shoot them down, there were too many this week.

There are no signs of Fed retreat and this is in the forefront of market participants’ minds. As 0DTE options retreat from the headlines so do all rallies it seems now.

The S&P also found support multiple times last week due to large options positions being hedged and rebalanced daily. But that dynamic dip-buying may be gone post expiration. One thing is pretty certain, any dip buying, if it occurs next week will be for the”right” reasons.

Gold and Silver: There is little new to discuss here. Now is the time to be patient. There is no asymmetry in this market currently. We’ve been all over these markets and anything we see out there is derivative of stuff we’ve diligently written on (Russia, China, Gold Standard, Physical demand, Bank lies etc) and alerted readers for the last year now. Gold and Silver have been in the forefront of many minds and center of many events this past 12 months. Right now, it is not. We briefly explain how we view that at bottom in a manifesto of sorts.

Broken Market 2023 Edition

Speaking of 0DTE options and their predecessors (illegally shorted stocks, exotics, HFT, marketmaker algos, 3x leveraged ETFs) as market moving items…

The very fact the stock market is being discussed in options terms more and more (like it was in meme stock terms in 2021, and HFT terms years ago ) is a horrible sign in our opinion. It is a sign the largest capital market in the world is increasingly being driven by various derivative users sometimes seeking to hide manipulative intents. And it is accepted by the regulatory agencies. The acute problem is now chronic. The new liquidity shenanigans compound on older uncorrected ones on regulators’ watch.

Stocks are a dog being wagged by numerous and evolving tails now. As organic flows shrink or move onto dark pools, the price action on lit exchanges has been more and more driven by esoteric assets and methods designed to capitalize on the missing organic liquidity. To drive the analogy home. The tail keeps getting bigger and more clever while the dog keeps getting smaller and less alert.

Finally and seemingly positive, Goldman notes investors' sentiment has turned much more bullish since the start of the year. If you believe as we do that this is in response to stocks having already rallied as opposed to economic prospects improving, you would think this not unlike retail buying Bitcoin at 64,000. Perhaps that is a little overstated, but it is in the same emotional neighborhood.

Finally, stocks also continue to be bullishly decoupled from The Fed's bank reserves.

Sector/Technicals

Energy was slammed benifitting neither from commodity risk, nor equities in genratl

Pharma was violently mixed, Defensives were good

Commodities:

The dollar ended the week modestly stronger despite selling pressure that started Friday in the European session.

Gold was down for the 3rd straight week (after rising for 6 straight weeks), unable to get back above $1900

NatGas prices fell for the 8th week of the last 9, closing at the lowest since Sept 2020

WTI closed the week lower, with a $76 handle

Copper was the only major commodity to make gains this week while PMs were down modestly, oil uglyish, and NatGas puked...

Bonds:

Bond were weaker with the longer bond slightly weaker than the short part of the curve- indicating very slight uninversion, but mostly noise and non-committal so far.

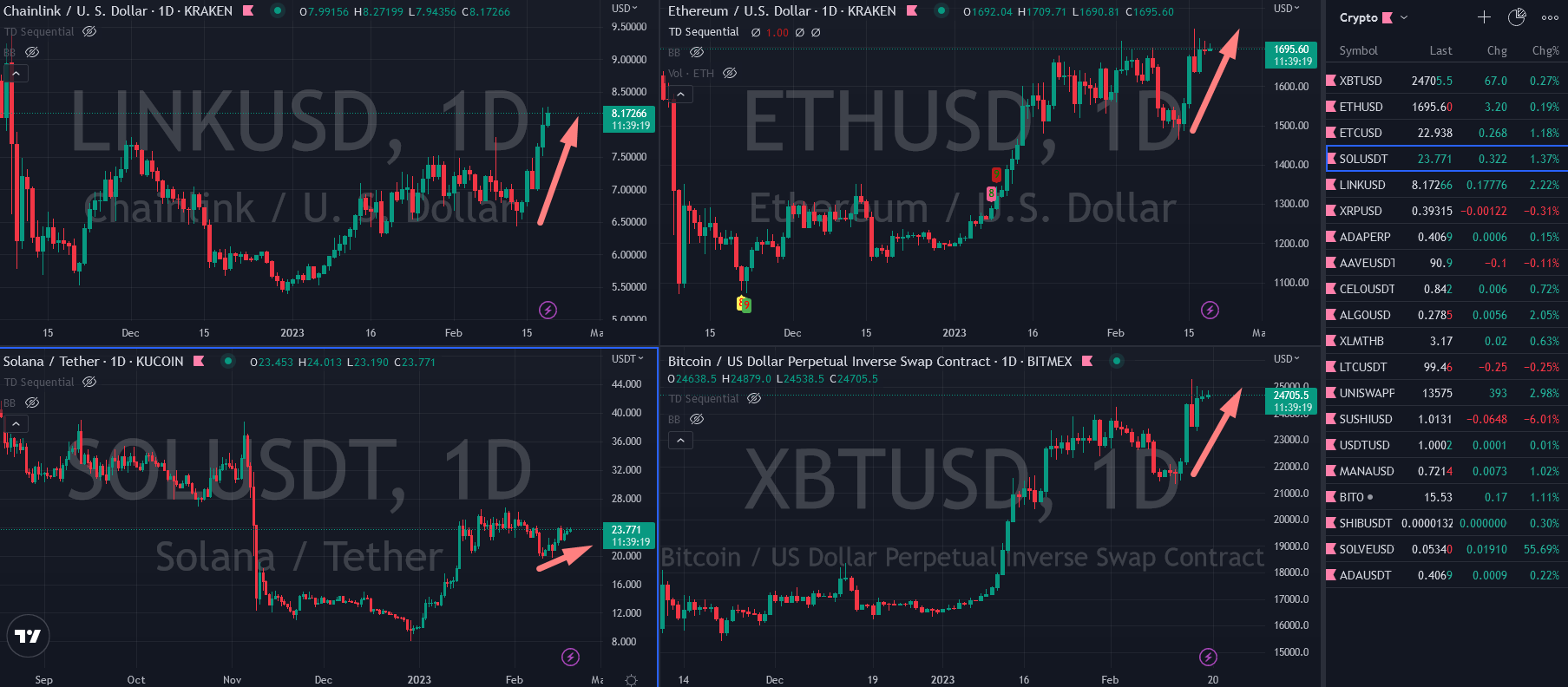

Crypto:

Bitcoin rallied over 12% on the week, its 4th weekly rise in the last 6 weeks, topping $25,000 intraday - the highest since June 2022

Ethereum also soared this week, topping $1740 intraday, its highest since Sept 2022

2. Research:

We have a lot today; none of which is Gold focused. Which is in part why we wrote what we did about Gold in our manifesto-like comment at bottom.

JPM, GS, TD, TS, Barc, Jeff on oil, Stocks, China, Macro, and Fed

MUCH MORE AT BOTTOM…

3. Week’s Analysis/Podcasts:

SPECIAL NOTE: Zoltan Gave us a Clue on the Current Situation

Exclusive-Brazil plans legislation to crack down on laundering of illegal gold