Weekly Part 1: This is What Happened at Silicon Valley Bank Friday

This is Why We Own Gold and Silver

Housekeeping: This Monday and every Monday we do a Silver/Gold podcast on Arcadia Economics. We request you take a look and subscribe to the other excellent silver-based content on that site. Much of the content in our podcasts builds on comments we make here on metals.

SECTIONS

Market Summary— Bank Crisis recap

Research— SUNDAY MORNING WITH GOLD RESEARCH ASWELL

Week’s Analysis/Podcasts— Banks, Gold, Silver , and more

Charts— Metals, Forex, Energy, Bonds, Crypto

Calendar— CPI, PPI

Technicals— GC, CL, BTC, SPX

Zen Moment— Gold looks good

Full Analysis— SUNDAY SUNDAY SUNDAY

1. Market Summary

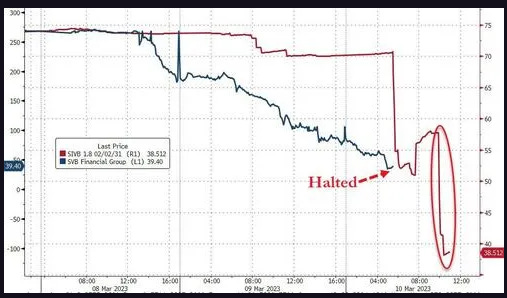

The week started out sleepy enough but late Thursday we got tremors in banking that decimated the industry’s stocks. Let’s just get to the main show, Silicon Valley Bank (SVB). Here is a play-by-play recap for Friday’s activity.

The stock was down over 60% before the market even opened in pre-market trading. Between 9:30 and 11:30 there were various headlines describing attempts to raise money and then to find a buyer. None were successful.

At 11:30 the headlines changed markedly from hope to despair. The FDIC closed the bank

*FDIC: SVB BANK CLOSED BY CALIFORNIA REGULATOR

*FDIC: SVB BANK IS FIRST INSURED INSTITUTION TO FAIL THIS YEAR

*FDIC CREATES A DEPOSIT INSURANCE NATIONAL BANK OF SANTA CLARA

*FDIC: NAMED FEDERAL DEPOSIT INSURANCE FDIC AS RECEIVER

*FDIC CREATES A DEPOSIT INSURANCE NATIONAL BANK OF SANTA CLARA

SILICON VALLEY BANK INSURED DEPOSITORS TO HAVE ACCESS MONDAY

And with that the US experienced its second largest bank failure in history. It was noted SVB’s stock price went from $763 to zero in 16 months.

The FDIC released a full statement. Here is an excerpt.

Silicon Valley Bank, Santa Clara, California, was closed today by the California Department of Financial Protection and Innovation…

All insured depositors will have full access to their insured deposits no later than Monday morning, March 13, 2023. The FDIC will pay uninsured depositors an advance dividend within the next week. Uninsured depositors will receive a receivership certificate for the remaining amount of their uninsured funds. As the FDIC sells the assets of Silicon Valley Bank, future dividend payments may be made to uninsured depositors.

Customers with accounts in excess of $250,000 should contact the FDIC toll-free at 1-866-799-0959- FDIC

There are so many second and third tier effects of this event as well as speculation that the bank-run was instigated by some well-heeled depositors and possibly even condoned by a large commercial banks like JPM.

Normally this would be conspiracy stuff. But it is not. We received and answered may questions on this. Here are the most relvant ones re-answered.

What happened to cause this?

Why was JPM poaching depositors before it went under?

This happened days after California and the broader US ended its Covid pandemic exceptions for bank risk- How much of that was a factor?

The FDIC took over very quickly. Quicker than Lehman. Why?

What will the Fed do with interest rates?

Did the SVB executives do anything?

What is one thing you can say with large confidence?

Is there contagion risk?

Anything Else?

Addendum

1- What happened to cause this?

First off the key here is banking reserves. A bank must have so much money in it at all times. Even if nothing is happening, if their loan portfolio drops, then their assets drop and thus their reserves drop. Regional banks are low on reserves right now. Meanwhile, the big banks have over $2TT in the Feds RRP program earning 4.75% or so.

SVB is a large bank but it is regional. Therefore it depends more on customer deposits than mega banks like JPM. A lot of their depositors are (were) tech company people in the San Fran area.

Commercial real estate crashed in the area, and is getting worse. They hold mortgages on these

The Covid pandemic emergency permitted banks to keep loans that were in arrears in the “ok” column. When that emergency was recently lifted, they had to then show they were losing money on defaulted mortgages etc…

QT and rate hikes hit tech stocks, forcing the bank to pay higher rates for deposits while customers drew down money- costs went up and deposits went down. (See here also)