Weekly: Russian Gold Use Banned By G7, US

URBAN EXODUS CONTINUES

Housekeeping: Many will be receiving GoldFix Weekly for the first time. It is different than the dailies. It is more like Barron's used to be. Content touches many areas of markets. The index may help.

**Founders class: How to build an Algo, Morning podcast changes, CoT, New Feature, and TraderSumo stops by to discuss past ME foreign policy and Technical Analysis Do's and Donts

SECTIONS

Market Summary DONE

Technicals DONE

Podcasts DONE

Calendar DONE

Charts DONE

Analysis:

Research:

1. Market Summary

The Bear market is over, the media would have you believe. Technically it is based on where stocks rallied to Friday. Forward-looking inflation expectations also dropped, Oil did a swan dive early in the week, Bonds stabilized, and stocks took the ball and ran higher with that info.

In a shortened holiday week, stocks snapped a major losing streak and averted being down for a record 11 out of 12 weeks. The reason was not due to economic optimism but in fact was because with a recession now assured, the Fed is expected to cut short its rate hike regime sooner than expected, most likely some time around the mid-term election.

Markets are now pricing in just a 71% chance of a 75bps rate hike in July, and are now tapering off rate hike expectations going out past September to the point that rate easing expectations are now creeping forward further into 2023. Dec and Feb rate hike odds plunged.

Powell’s focus now is solely on inflation, but it is not so much on the actual number as it is on his fear that inflationary expectations will become entrenched and give rise to wage-price spirals. These then can become out of control in a self-reinforcing cycle.

In short, he is worried more about what people think of the future than about how prices are bad now. Which is why markets were so focused on the UMICH inflation expectations report.

While the market's realization that a recession is now the baseline certainly helped, it was the unexpected news from the final UMICH inflation expectation print for the next 5-10 years, which was revised down from 3.3% to 3.1%, meaning that the "unanchored" inflation expectations that Powell saw and was freaked out by (his own words), never actually happened and was revised away before it even hit the history books.

There are a couple observations, not necessarily related to each other on all this Fed Drama possibly worth mentioning.

The Fed is more concerned with managing inflation expectations than the inflation currently in the economy.

If the Fed turns its attention to the recession ( most now believe we are already in) from Inflation, then stocks will continue to rally.

Oil rallying with stocks on Friday says inflation is just not contained yet.

Market behavior is already turning from QT behavior to QE behavior

There are far too many shorts in stocks again that will be gasoline on the fire the next week or so.

If Oil continues to rally, we feel the Fed will not back off it’s inflation fixation. Thus stocks would be making a mistake thinking the Fed is dovish again until oil drops and stops.

“The scheduled events of Saudi production, SPR sales ending, and expected ramp up in US production are all converging in the fall. All (not?) coincidentally while maintenance season starts. So to the extent that the Saudis play well in the sandbox that will go smoother. But most importantly, US production has to catch up or the other pieces do not come together”- Brynne Kelly

It remains as it has been for the past year. Oil is the key to this next cycle.

If Oil does not drop for a reason beyond Fed behavior like War ending or some other supply increase, Powell is trapped.

Until later in the summer, the rally may continue unabated as a generation of stock “investors” has their hopes spring eternal again.

We’re watching oil and think until there is a financial crisis as there always is in rate hike cycles, stocks will rally until they do not. Every rally will continue to be met with tough talk until something truly breaks again.

The fact that oil is bouncing hard on Friday suggests that traders are already starting to price in the coming Fed easing which will slingshot commodities even higher. Then Powell has a problem.

H/t Newsquawk and Zerohedge for data and some graphics.

Sectors:

Every single sector closed solidly green on Friday

Duration is back as tech stocks outperform basic materials and energy on the week

Energy stocks - remain the best performing asset and sector of 2022

Commodities:

Friday’s meltup was enough to almost undo the week's rout in oil, which after plunging 7.5% last week, and slumping earlier this week, staged a dramatic bounce on Friday, rising as much as 3%, and just barely closing red on the week.

Bonds:

CPI-shock yields have drifted sharply lower and are now just fractionally higher compared to where they were before the "blackout period" CPI prompted Powell to panic.

Rate hike expectations and rate cut hopes are what drove stocks higher not economic recovery

Crypto:

Crypto moved sharply higher, with Bitcoin well off last Saturday's lows. Much bad news is out, bad players have been rescued, Saylor bears have been slapped, and the market looks to want to reassert its ties to tech stocks again.

We’ve noted a wild divergence in market participant opinions now; some calling for $11,000 in a heartbeat, others calling for a “skate right up to $29,000 now that the Celsius bad news is out.

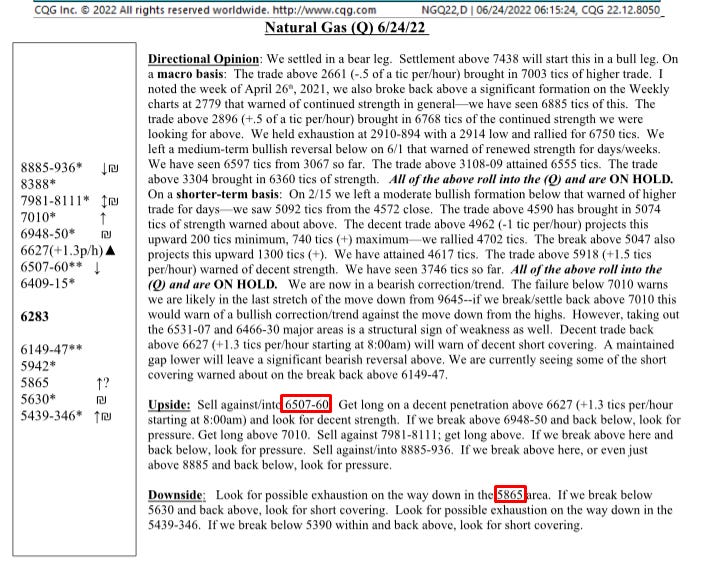

2. Technical Analysis

Report Excerpts Courtesy MoorAnalytics.com

GoldFix Note: Do not attempt to use price levels without symbol explanations or context. Moor sends 2 reports daily on each commodity they cover. The attached are non-actionable summaries.

Gold

Between $1861 and $1816 all macro structures will be on hold. Trade as you normally do in that range

TECHNICALLY BASED MARKET ANALYSIS AND ACTIONABLE TRADING SUGGESTIONS Moor Analytics produces technically based market analysis and actionable trading suggestions. These are sent to clients twice daily, pre-open and post close, and range from intra-day to multi-week trading suggestions. www.mooranalytics.com

Energy

We just finished a major bull formation, expect rallies to be sold

Below $107.05 will find repeated selling of strength, watch spreads

Bitcoin

Go to MoorAnalytics.com for 2 weeks Gold, Oil, and Bitcoin reports free

3. GoldFix and Bitcoin Podcasts

Goldfix podcasts have been for the last year or so a mix of market observation, Gold education, and actionable trade ideas using Moor’s Technical analysis as a basis for discussion. Given the recently added content: Research, writers, and this winter’s academic curriculum, we thought active traders were getting the short end of the stick. Therefore we sought to rebalance the content.

For the next few months it will focus on actionable trade ideas from our own activity in Gold, Silver, Oil, Bitcoin and ES Futures. Premium subscribers will have access.

The ideas shared/discussed will be based on our own analysis and game plans shared with subscribers. They will not be trade recommendations for viewers, but a view into professional preparation, process, and starting points for active traders to form their own ideas. Trade ideas will be both bullish, bearish, and neutral. They will also be short term in duration. Even if you do not trade this way, the risk mgt aspect may be helpful in wiring your own brain for markets.

GoldFix Broadcasts HERE

Bitcoin Podcasts HERE

4. Calendar

Some upcoming key data releases and market events

MONDAY, JUNE 27

8:30 am Durable goods orders May 0.2% 0.5%

8:30 am Core capital goods orders May -- 0.8%

10 am Pending home sales index May -4.0% -3.9%

TUESDAY, JUNE 28

8:30 am Trade in goods (advance) May -- -$105.9 billion

9 am S&P Case-Shiller U.S. home price index April -- 20.6%

10 am Consumer confidence index June 101.1 106.4

WEDNESDAY, JUNE 29

8:30 am Gross domestic product revision (SAAR) Q1 -1.5% -1.5%

8:30 am Final domestic demand revision (SAAR) Q1 -- 2.7%

8:30 am Gross domestic income revision (SAAR) Q1 -- 2.1%

THURSDAY, JUNE 30

8:30 am PCE inflation (monthly) May -- 0.2%

8:30 am Core PCE inflation (monthly) May 0.4% 0.3%

8:30 am PCE inflation (year-over-year) May -- 6.3%

8:30 am Core PCE inflation (year-over-year) May 4.7% 4.9%

8:30 am Real disposable income May -- 0.0%

8:30 am Real consumer spending May -- 0.7%

8:30 am Nominal personal income May 0.5% 0.4%

8:30 am Nominal consumer spending May 0.4% 0.9%

8:30 am Initial jobless claims June 25 227,000 229,000

8:30 am Continuing jobless claims June 18 -- 1.32 million

9:45 am Chicago PMI June -- 60.3

FRIDAY, JULY 1

9:45 am S&P Global U.S. manufacturing PMI (final) June -- 52.4

10 am ISM manufacturing index June 54.9% 56.1%

10 am Construction spending June 0.4% 0.2%

Main Source: MarketWatch

5. Charts

Gold

Silver

Dollar

Charts by GoldFix using TradingView.com

6. Analysis: GoldFix Commentary

We held off on sending the report until today so as to digest the breaking news on Russian gold exports. Here are the most relevant headlines:

G-7 TO ANNOUNCE IMPORT BAN ON NEW RUSSIAN GOLD: US OFFICIALU.S. PRESIDENT BIDEN AND G7 LEADERS TO AGREE TO IMPORT BAN ON NEW GOLD FROM RUSSIA -SOURCE FAMILIARThe News

You can read the story in many places as we did. We read the versions in Barron’s, Reuters, and several other places for clues as to probability and rollout time frame. Most had their coverage of it with little meat or conjecture on what will happen to Gold itself. As of this post, there is no research out through Sunday. We get a lot to look at.

The Bottom Line

The Gold Market will now be more like oil. more expensive in the West and cheaper in the East Biden's decision will make the gold market bifurcate: cheaper for Russian-friends to buy and much more expensive for Russian enemies. it may make related selling move West for better prices, but it won’t impoverish China that’s for sure.

The Narratives

You can expect several narratives to pop up in the Gold community now.

Gold is going to the moon

The Comex will break now

Gold is going to zero

All of those are possible, some simultaneously. Few of the people saying it to our ears have thought it out yet. We have strong opinions but do not announce them here. Everything is about probabilities, Value at Risk, and who the weakest hands are now.

All trades put on for probability reasons will be taken off for VaR reasons now. Translation: I want my money returned to me, and do not care about my return on money potential. as the saying goes.

No sense in writing opinions as the news is just being digested. Opinions are expressed in trades. The news will only harden what you already believe. Hopers will hope, deniers will deny. Everything is tactical now.

So here are what we think are reasonable, not necessarily obvious, and hopefully insightful comments to help you decide what to do, if anything.

If you have nothing to do, then good for you. Sit back and watch to see how these factors play out. They will play out, not all continuously or simultaneously, but they will play out.

So we thought the best format to do this in would be to list simply the top 3 immediate risk players of the event, and then bullet our notes rather than writing a story. What we’d suggest is read and assume the comments are from a thoughtful place. Decide to what extent you agree with them, and weigh your own decisions based on what you think the outcome will be.

We will answer questions in the comments section.

Many of these concepts have been discussed in past posts. But to see them snap into place in one event is what it is all about for us as risk mgrs. One more thing, we think more Russian Oil related news is coming, but cannot be sure.

What follows was the essence of our own risk morning meetings for traders. It is a good way to start thinking about the future of Gold even if you are not trading….

Continues at Bottom7. Research:

Normally we look for what we think is relevant to the economy and Gold. It is very notable that for 3 weeks running there is a complete dearth of Gold analysis. Now we may know why. This is not paranoia, it is common sense.

Gov’t, when it is about to make a move always asks banks to hold off on publishing certain things. We think ( but cannot prove) that is what is going on now. As detailed as the Oil coverage has been due to the war, the Gold coverage has been abyssmal. Oil coverage also dried up this week as well.

We are reminded that in the run up to Iraq 2, the Fed asked refiners to secure new sources for production weeks before the invasion. So this is not simple speculation. Don’t be suprrised if big Oil news drops from the G7 as well.

Today we share: JPM, DB, GS, Comex rules, SG, and more. Crypto, Economics, Urban flight and possible bear market death are on the table. But zero good metals stuff. And zero from the dynamic duo in commodities: GS, JPM,…. that says a lot maybe.

Continues at Bottom