What's the Real Reason Powell isn't Cutting?

Hint, It's Not Tariffs

Since Donald Trump took office and the tariff/trade war became a focus of finance, Jerome Powell has made it a point to use the uncertainty around the implementation of Trump's policy as a reason not to cut rates. This was a seemingly legitimate reason for quite some time.

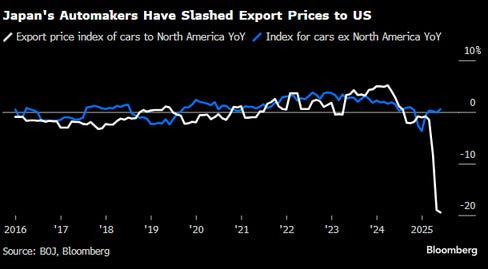

Recently, however, that reason—“uncertainty”—is less true. Specifically, the Fed Chair himself stated that uncertainty is a little bit less uncertain most recently. In fact, the data shows that tariffs thus far have been disinflationary, as companies and nations are absorbing the increased costs associated with them. Japan would be the biggest and best example.

Further, the daily real-time data, which had been decidedly exhibiting a recessionary vibe, has finally been joined by the hard, monthly data that Powell focuses on after errors made during Covid.

So if Powell is less uncertain about tariffs, and tariffs themselves are at least not inflationary yet, then why is Powell so reticent to cut rates, given that the recessionary path is clearly close to being at hand? We have offered the following reason: