When the Hedge Needs a Hedge

GFN – NEW YORK: Several asset managers have reduced exposure to gold mining equities after the shares began trading with meme-stock volatility that has decoupled them from bullion and undercut their traditional role as defensive hedges.

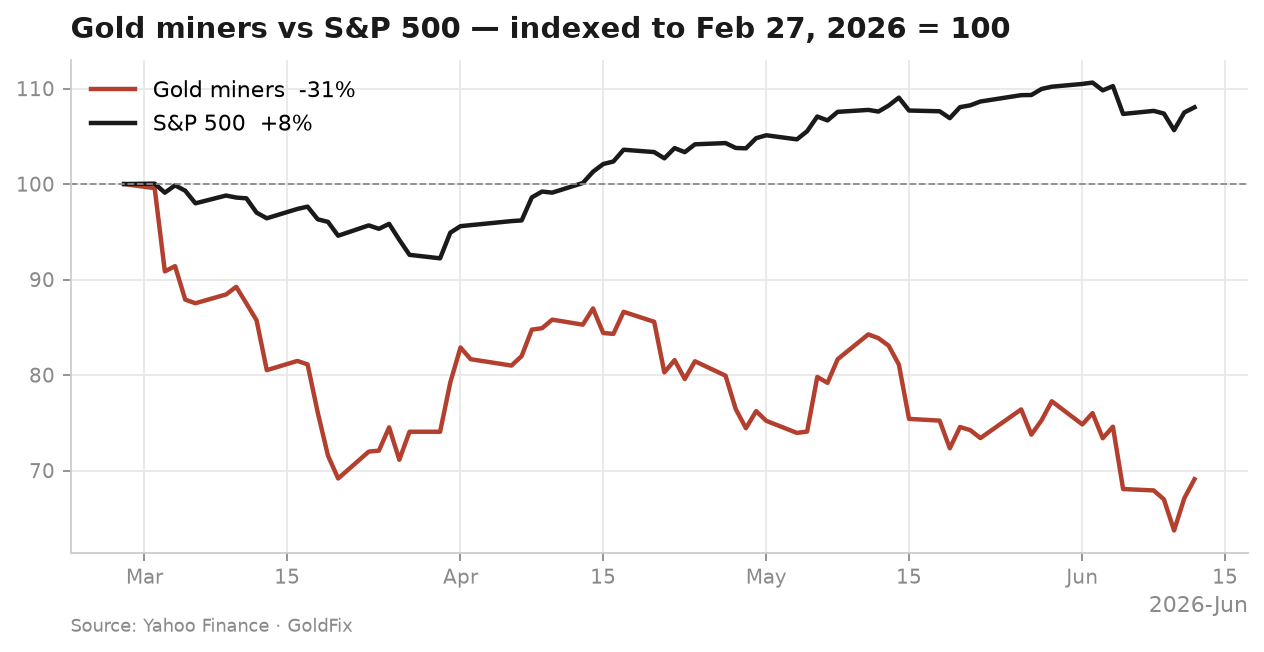

A NYSE gauge of gold miners has fallen 31 percent since the end of February, while the S&P 500 Index has gained 8 percent over the same period, according to Bloomberg News, a divergence that has accompanied sharp, headline-driven swings across the mining complex. Brian Laks, chief investment officer of Old West Investment Management, has been trimming the Los Angeles firm's gold holdings after bullion and related shares rallied to records and began behaving like speculative instruments, a shift from the defensive role they long played.

The shares have tracked the course of Middle East diplomacy in recent sessions, falling 4.8 percent on a Wednesday after renewed threats of US strikes on Iran, recovering the next session once those strikes were canceled, and closing 3.6 percent higher on Friday amid reports of progress toward a US-Iran agreement. Other managers have moved similarly, with Tuttle Capital Management cutting its gold and silver allocation to 5 percent of its actively managed fund from about 15 percent since the conflict began, and the VanEck Gold Miners ETF recording three consecutive months of outflows.

"Gold's not the same trade that it was 10 years ago," Laks said.

The repricing follows an exceptional run, as gold gained 65 percent in 2025 and the NYSE gold miners index rose 155 percent, with Newmont, Barrick and Agnico Eagle each advancing at least 116 percent, leaving the group sensitive to shifts in risk appetite. The retreat has unwound part of that advance and left miners trailing the broader equity market, a divergence that has tested the sector's long-standing reputation as a steadier proxy for the metal. The episode reflects gold's evolving function within institutional portfolios, where a former haven asset is increasingly assessed alongside higher-beta equity exposures.