Good Morning. As mentioned, we are mostly out of pocket this weekend. No Founders discussion either for the same reason unfortunately. Plenty to read below however. As usual, Full analysis at Bottom

Hartnett on Fiscal Irresponsibility

HSBC Shows us the Shortages

JPM Cancels Recession Call

TD: CTA Gold report

GS Weighs in on CPI

Connection between CRE and Small Banks*** by request

More…

Some interesting excerpts.

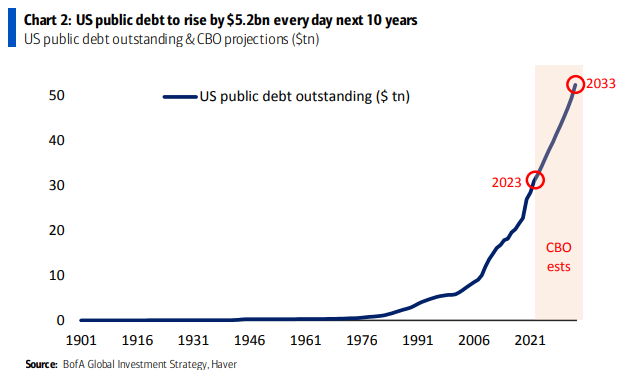

Hartnett: not a lot of color compared to last week.. but what he does say is pretty harsh…

Debt downgrades ≠ fiscal discipline; central banks still in business of bailing out Wall St, governments very much in business of bailing out Main St

...ultimately policy destination is Yield Curve Control across G7 once next recession provokes fiscal policy panic & even higher government default risk.

COMMENT: This is what YCC looks like if Hartnett (now in agreement with our long lost Zoltan) and Goldfix (YCC is here) are correct.

PLENTY MORE ON YCC, FINANCIAL REPRESSION, AND INFLATION HERE

HSBC Commodity Report (great all in one report for the supply side of things). but mostly Energy and Grains

Softer US CPI supported gold prices Gold prices rose slightly, on average, in July 2023. It appears that gold prices were supported in June by signs of slowing inflation in the US. Early in the month, the US CPI rose by its smallest rate in 2 years, up by 0.2% m-o-m and 3% y-o-y in June, which saw a pullback in yields and a weaker USD, supporting gold. This theme was evident later in the month too, with core PCE rose 0.2% m-o-m and 3% y-o-y, the ECI rose just 1% q/q and 4.5% y/y in Q2. Elevated geopolitical risks are also likely supporting gold prices. HSBC expects gold prices to average USD1905/oz in 2023 and USD1850/oz in 2024 (previously USD1820/oz; see ‘Gold Outlook: Gold recalibrates lower’, 5 July 2023).