Weekly: Mining Industry Ripe for M&A

Also: Soft Landings Don't Kill Inflation

Housekeeping: Many readers here hold mining stocks. Must read for those who have industry positions in Gold, Copper, and Silver. Gold and Copper will increasingly be linked at the mining business level for multiple reasons… Going forward, due to growing content responsibilities, the weekly report, for over a year our 2000+ word work of passion, will have to be reduced to make room for write ups readers prefer and time constraints.

SECTIONS

Market Summary— Half measures do not work

Research— M&A is going to ramp up

Week’s Analysis/Podcasts— China, Pozsar, CNBC

Charts— metals, energy, and FX

Calendar— GDP, PCE/UMich

Technicals— GC, CL, BTC, SPX

Zen Moment— Nice Watch

Full Analysis— TD, JPM, GS, BOA

1. Market Summary

"Every time the Fed softens the [rate hike] path just a touch, commodities are back in their face in a heartbeat.” — London CIO

Despite Friday’s surge, stocks ended the week lower (Dow in the red YTD) with Nasdaq up and the Dow down 3% on the week. What is different in the rally this Friday was what lead things higher and what that implies.

When stocks dumped, they all dumped last week. When stocks rallied, Tech lead. This strongly suggests in combination with other information we saw, that investment allocations are just getting going in being rotated/redeployed into stocks.

Mind you, stocks were down and weaker in general most of the week; but behavior Friday on the back of Google and Netflix— where the former was rewarded with a rally for laying people off, and the latter exploded higher despite missing earnings (but guiding their ad-product doing well)— hints at bottom fishing arriving. Then the Fed talking dovishly even as stocks rallied gave even more impetus for sidelined money to step back in.

ROTATION INTO TECH AGAIN?

The net result was all stocks dropped on bad earnings news as we thought would happen. But tech rallied quite nicely for reasons described above while industrials languished. Money managers are now looking to put stock money to work more aggressively.

This augurs for at least a couple more days of buying and rallies. The question will then come back to two things afterwards: The first is easily seen: What will the debt ceiling nonsense do to markets? The second is something we are trying to handicap.

FED PIVOT OR PAUSE

Specifically: Is the market now discounting a Fed doing a 180 from hiking to lowering rates, or are stocks beginning to price a Fed moving rates sideways for some time after reaching their peak. We don’t know. But we do know this. Every time dovish behavior happens in Fed land, Commodities are as strong if not stronger than their stock counterparts. Goods inflation is not dead.

What do we mean? This hiking cycle had a pronounced effect on goods inflation, mostly energy related goods. Thus commodities (raw goods) dropped precipitously during the rate rises, which was their stated goal. So far so good. While stocks took it on the chin during the hikes, commodities also got pummeled.. BUT…..

COMMODITIES ARE PERCOLATING AGAIN

In the recent Fed dove talk, commodities have rallied every bit, and then some as stocks did. Goods inflation is not killed at all. It is merely sleeping.

And that is very bad if you are rooting for the Fed to generate a soft-landing with inflation left for dead.. Why? Because stocks are bouncing at a much slower rate than inflation is in anticipation of Fed dovish behavior. If Powell & Co. are looking at it like we are, then there will be no u-turn from hiking to easing.

Remember, this cycle was not unlike chemotherapy racing to kill an inflationary invader before it killed the economy. We said in June’s What is Going On Right Now?

Put more simply: the intended consequence of slowing inflation by raising rates is having a much more exaggerated effect on the economy before it fixes the inflation. An insensitive but very appropriate analogy is this: The chemotherapy is killing the (unhealthy) patient faster than it kills the cancer.

So: the economy has survived, inflation is on the wane. Goods (energy) inflation is lower, and Services (housing related) inflation is now coming down nicely. But it ain’t dead at all. clocking in at 6% is not dead by any stretch. Be ready to start hearing talk of 2% to be in our sites again.

But we think of it like this for now:

If: the Fed stops hiking

And: both stocks and commodities continue rallying again

Where: inflation data remains subdued for a while because lagging stuff like housing is just starting to hit lower.

Then: commodity price increases will be more tolerated by the Fed as long as the “services “ part of inflation remains subdued.

But: if services inflation turns upward again, its game over for this thesis.

Put concisely: The Fed will not give a damn about oil or food or copper as long as the inflationary pressures from housing services are still manifesting. Call it what it is. Further, even with a stingy Fed, the Chinese reopening will keep a bid under commodities somewhat. Covid 2.0 invalidates that of course.

Everything got hammered, Commodities are bouncing better…

Therefore: The risk/reward between stocks, commodities, and bonds is to again be long industrial/consumed commodities. Keeping in mind if the Fed remains stingy, they will definitely get hit again.. but we’re betting not like stocks will get hit. The play may be to be long commodities, and short industrial stocks.

Examples of commodities off their October lows according to Bear Traps: : Iron Ore +48%; Silver +38%; Copper +35%; Uranium +32%; Aluminum +25%; Corn +20%; Gold +19%; Sugar +14%; Coal +8%; Wheat +2%

Soft Landings Don't Kill Inflation

Circling back to our chemo-to-kill-inflation analogy… You cant kill inflation with half measures. And if we get a soft landing for stocks/ economy. We *will* get goods inflation returning with a vengeance. Here’s Larry Mcdonald of the Bear Traps Report again:

"Soft landings" have NEVER killed inflation, not in the history of mankind. If a soft landing is your base case for higher stocks, the Fed has to do a lot more.”

On that note: we are long some oil in ETF form, BTC/ETH (as our tech stocks with monetary qualities), and just rebought tiny Silver speculatively using Tech levels from Moor in Gold (above 1920 puts 1980 on radar). We think Silver can hit $26 if gold holds. But its just a trade, not an investment. These are 2 week to 2 month trades with room to add if things drop from Debt ceiling stuff, but not to add if Fed starts talking tough again. The other known event risks are:

Chinese New Year— could be very bearish Gold

Debt Ceiling— bullish Gold

Good luck

Sector/Technicals

Tech did extremely well as markets started aggressively discounting rate hikes ending

Technical levels dominated price action this week with the S&P breaking below its 200DMA and then trading around its 50DMA.

Commodity/Energy did well in sympathy with China reopening and Fed kindness

Nasdaq flip-flopped between its 50- and 100-DMAs

Consumer defensives, Industrials, Utilities got hit as symptoms of flight from safety risk-on behavior took control

Commodities:

The Dollar ended the week very modestly higher after some noise midweek shifted the greenback out of its narrow range

Gold closed the week at its highest since April 2022, finding support at $1900 numerous times

Commodities were broadly higher on the week with Oil, Gold, and Copper all higher while NatGas ended lower

Gold closed the week at its highest since April 2022, finding support at $1900 numerous times

Bonds:

Treasuries were dumped for the last two days, erasing the gains from the start of the week and dragging 30Y Yields higher on the week (as the short-end outperformed)

At the shortest-end of the curve, the T-Bill curve is starting to 'kink' around the June/July period in anticipation of the debt-ceiling debacle

Crypto: Tracking Metals or Stocks now?

Last week we noted Crypto was late to the party but tracking Metals.This week we add to that.

Cryptos rallied this week with Ethereum outperforming Bitcoin (and Solana leading them all)

Metals/Crypto share monetary qualities. Crypto/Tech stocks share speculative qualities…. Crypto is now tracking stocks when they rally from perceived Fed kindness as well now.

H/t Zerohedge for data and some graphics.

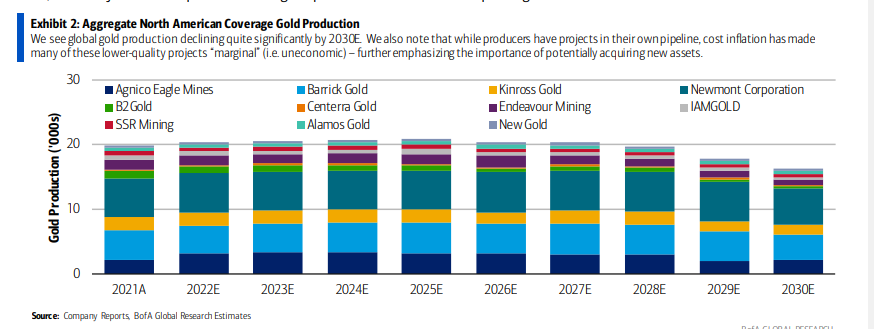

2. Research Excerpts: Miner Must Read

BOA returns again with yet another Gold report. This time it is on miners specifically looking at potential M&A activity. We find this extremely interesting for those of you in the mining sector and can explain our interest in 3 sentences.

Here’s the meta take that matters:

When a bank is contracted or believes there are undervalued companies in the industry they do their research on the business (gold) and the companies

They put out public reports first on the industry, like this one. And then on the companies within it.

Something possibly happens in M&A in 6 months to a year.. We know something of M&A behavior from Lehman days

Topics discussed include:

M&A is a growing necessity…

Who might be the acquirers?

Gold price volatility in 2023 not necessarily a deterrent

The case for big (and bigger) gold still exists

Plus More…

CONTINUES AT BOTTOM…

3. Week’s Analysis/Podcasts:

Special Message To GoldFix Readers of the Precious Metals Persuasion

Some Basics Regarding PetroDollar Death and Gold Backed Currencies

Pozsar: Great power conflict puts the dollar’s exorbitant privilege under threat

BREAKING: CNBC says Silver prices could touch a 9-year high in 2023

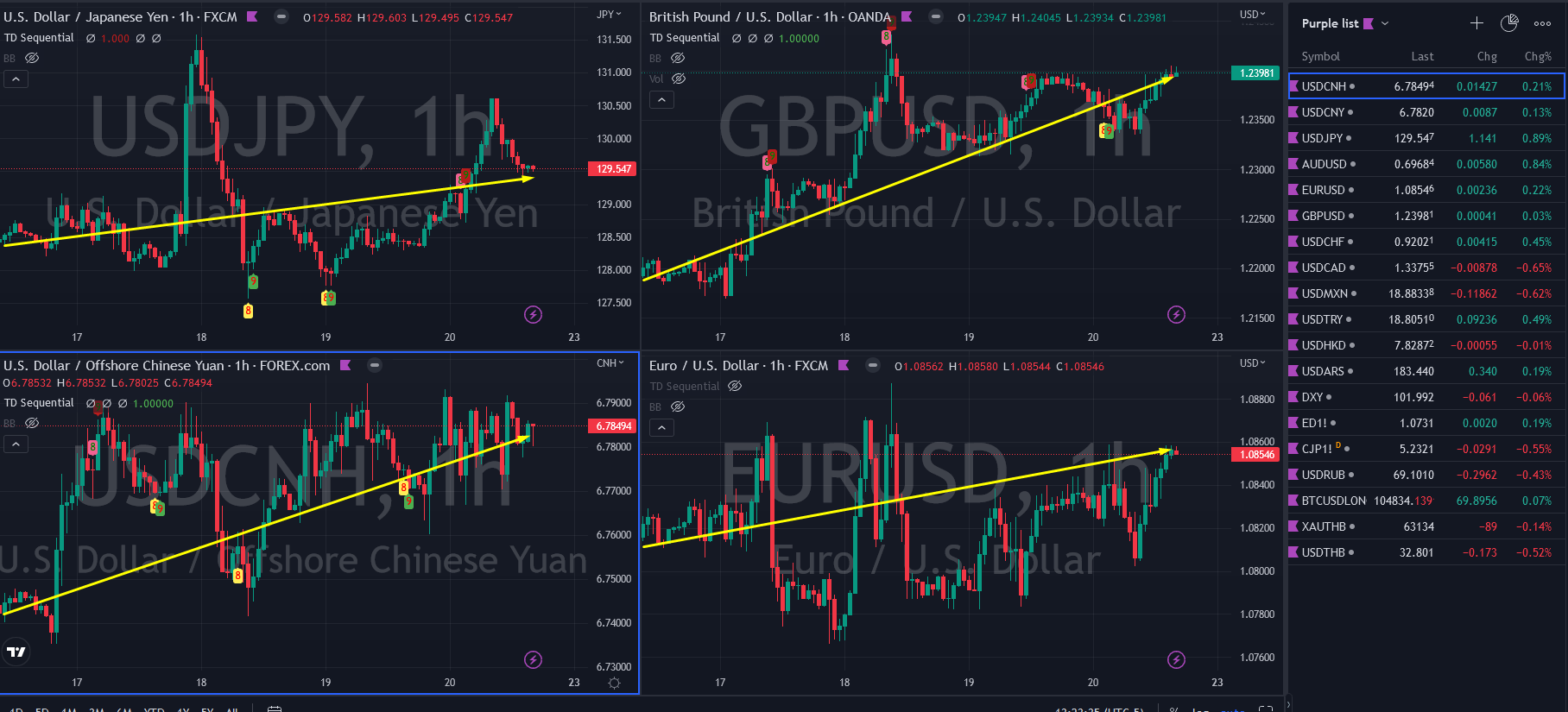

4. Charts:

Metals and DX

Metals/PGMs

Energy

Forex

5. Calendar

MONDAY, JAN. 23

10 am Leading economic indicators Dec. -0.7% -1.0%

TUESDAY, JAN. 24

9:45 am S&P U.S. manufacturing PMI (flash) Jan. 47.0 46.2

9:45 am S&P U.S. services PMI (flash) Jan. 45.3 44.7

WEDNESDAY, JAN. 25 None scheduled

THURSDAY, JAN. 26

8:30 am Initial jobless claims Jan. 21 199,000 190,000

8:30 am Continuing jobless claims Jan. 14 -- 1.65 million

8:30 am Real gross domestic product, first estimate (SAAR) Q4 2.8% 3.2%

8:30 am Real final sales to domestic purchasers, first estimate (SAAR) Q4 -- 1.5%

8:30 am Trade in goods (advance) Dec. -- -$83.3 billion

8:30 am Durable goods orders Dec. 2.9% -2.1% 8:30 am Core capital goods orders Dec. -- -0.1%

8:30 am Chicago Fed national activity index Dec. -- N/A

10 am New home sales (SAAR) Dec. 615,000 640,000

FRIDAY, JAN. 27

8:30 am Real disposable incomes (SAAR) Dec. -- 3.2%

8:30 am Real consumer spending (SAAR) Dec. -- 0.1%

8:30 am PCE price index Dec. -- 0.1% 8:30 am Core PCE price index Dec. 0.3% 0.2%

8:30 am PCE price index, year-over-year Dec. -- 5.5%

8:30 am Core PCE price index, year-over-year Dec. 4.4% 4.7%

10 am UMich consumer sentiment index (late) Jan. 64.6 64.6

10 am UMich 1-year inflation expectations (late) Jan. -- 4.0%

10 am UMich 5-year inflation expectations (late) Jan. -- 3.0%

10 am Pending home sales Dec. -1.5% -4.0%

Main Source: MarketWatch