HouseKeeping: Good Morning. Several posts today. This one is a long detailed read about how naked short selling of stocks is finally being pushed back against by the investor community. If you are pressed for time today, the summary will do.

Without the big banks and financial institutions’ complicity, this highly destructive form of naked short selling [rehypothecation] could never happen.

Contents:

How Rehypothecation Ends

Is This The End Of Naked Short Selling?- pdf

Summary:

The story attached at bottom is an extremely important step in addressing long standing inequalities in the Precious metals markets surrounding rehypothecation of futures although it is about stocks.

The story attached below is important for several reasons, not the last of which is the end of naked short selling, a cousin of Metals Rehypothecation

The courts are now being made aware of the criminality surrounding naked short selling of stocks. In doing so, they will also draw unwanted attention to the long-standing practice in precious metals (and other futures) of the same practice. This practice is known as rehypothecation in the physical world. In Equity-Land they call it naked short-selling. And it is illegal.

In Stocks, Shorting what you do not have is illegal…

In equities, you may not short a share of stock that does not yet exist. This protects the company from pile-ons where people with unlimited means can (and would) short a stock more than its actual share float. Sound familiar?

It is important to note that shortsellng itself is not illegal. The stock market currently regulates legitimate shortselling by allowing longs who actually make their shares available to be shorted charge interest for that privilege. This is enables a “covered” short sale and protects a company from unwarranted pile-ons while allowing traders to bet on the company not performing well in its business.

Sounds fair right? Here’s where it gets sketchy, and dodges the intention of the post 2008-09 ruling against naked shortselling.

…But Banks found a way around that rule.

There are regulatory loopholes that large predatory funds and banks take advantage of, wherein they can short stocks that have no shares available for “covered” short selling. This gives them the ability to bet on the short side unlimited money, even when the float of a company is significantly less than unlimited. The article gets into the details of how that actually manifests.

For this summary, know that the institutions benefiting from these loopholes create “ghost shares” to be used for illicit naked shorting.

Death Spiral Financing: “We’re Here to Help”

Not infrequently this can manifest in a game called Death Spiral Financing1whereby the short-selling entity “rescues” the shorted stock by offering the company new terms for refinancing their business after the price has collapsed. Those new terms will necessarily entail issuing more shares. The newly issued shares are then bought by the ”rescuer” (frequently in a private placement) who uses them to cover his predatory shorts2.

Precious metals investors know this all too well. Shorts use the long-liquidation to cover their own short-selling almost daily.

The End of Rehypothecation?

Eventually questions will come up that matter for metals people as this illicit practice is made expressly illegal:

Why is it Ok to short commodities you do not have available for delivery?

Why is it ok to short something physical you do not have access to?

Then we may see a wholesale restructuring of the futures market. This will not happen for years officially. We suspect, based on our understanding and experience studying these types of phenomena, the market will “fix” this long before then by completely de legitimizing Comex and moving all domestic trading of precious metals onto the ETF side organically. But that is another conversation.

[B]anks have been managing their paper gold books with one assumption, which is that [Nation] states would ensure gold wouldn’t come back as a settlement medium.

But, Gold *is* coming back as a settlement medium. And the past year we’ve seen the banks scramble for the shrinking above ground metals collateral that is available in an attempt to unwind their decades of positioning this way.

For now, know the Bullion Banks are already finding someone to hold their short bags and stop them out at as we speak. That is manifest when a failed Comex delivery is stopped out and absorbed by a Bullon bank. Another comversation on that someday3.

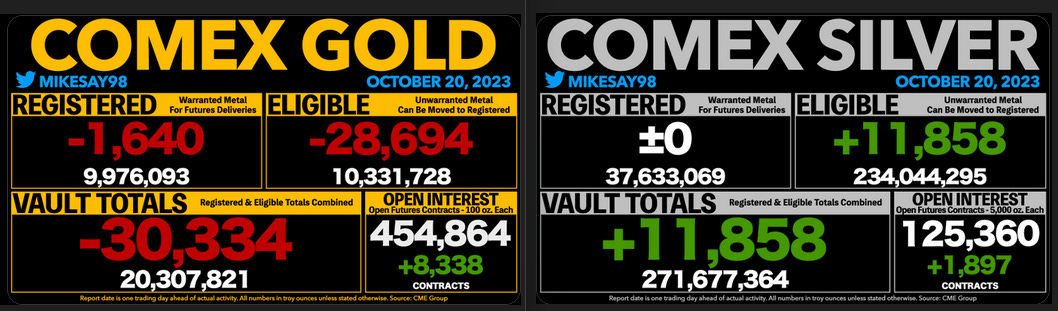

As of Friday:

- GOLD FUTURES: Open Interest is now equal to 224% of all vaulted gold and 456% of Registered gold.

- SILVER FUTURES: Open Interest is now equal to 231% of all vaulted silver and 1,666% of Registered silver.

Anyway.. with deglobalization and the end of easy access to collateral, leveraged financing of shortside trading is ending. Which means there is simply no metal for shorting available, and rehypothecation will die.

If you want to learn more about this strictly from a precious metals POV, we strongly urge you to revisit the post below. In it, Pozsar painstakingly describes the path we are currently on.

Housekeeping/PSA:This was written on December 26th for GoldFix subscribers and was unlocked because it may be too important to keep under wraps. This is parts 2 and 3 of a premium post. Part one was shared with ZeroHedge readers Dec 27th (link at bottom). Last night we read ZeroHedge's 5800 word analysis and explanation of Pozsar's Dec 27th missive on r…