Weekly: Ukraine We Have a Problem

Goldman, Bloomberg, and more

Housekeeping: Founder’s Class will be 3 p.m. SATURDAY due to Football. Zoom Link Here. We will focus on updating our CoT analysis for handicapping next week’s markets. Founders use usual password please. See you then.

This is a long, dense post intended to be read like a weekend magazine or a Sunday paper. Please note some sections have changed order.

SECTIONS

Market Summary: weekly recap

Technicals: active trading levels

Podcasts: GoldFix and Bitcoin

Calendar: next week

Charts: related markets

Premium divider

Precious Research and Analysis

Premium Reports - Commodites, Backwardation, and Positive Interest Rates

1. Market Summary

we know.. it’s a horrible title.. sorry. lol

On Thursday, the Fed made it clear it was serious this time about raising rates and withdrawing liquidity. On Friday, the Ukraine fears began being taken seriously as well. Next week we have a lot of serious vectors being managed by conflicted people. Full blow-by-blow commentary beneath the fold how we got here. First the markets.

pre cpi is the jobs data happiness

post cpi is a market more worried about inflation

war… hikes may not happen yet again.

For here, let’s focus on Friday.

The U-Mich sentiment report came out. It showed a deteriorating economic optimism and persistent growing inflationary fears. The markets took the inflationary part to heart. First: Why is this U-Mich report important?

The reason this report is taken so seriously; it is one of the few, if not only, report that looks forward. Every other data point is backward looking. This is a glimpse into what the people who determine the economy actually feel. And this Friday, they felt badly.

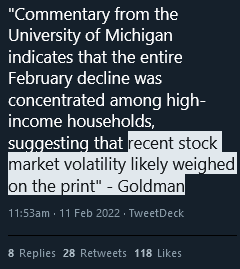

The report came out at 10a.m. We quickly surmised the UMich report was worse than it looked and at 10:08 a.m. we posted this on twitter.

Note our phrase: “stock volatility is not good for economy”.

Here’s why. The U-Mich kicker was inflationary fears were from people making OVER $100,000 a year. These people have no real worries about inflation presently. But.. and this is a big but.. their portfolio and spending habits are linked. That means they spend less, invest less, and wait longer. The engine of everything is getting apprehensive. We thought that was very bad. It means the fear (real or imagined) is spreading up the economic ladder now. Then at 11:53 Goldman said this:

We don’t know whether to be flattered or worried by this GoldFix/ Goldman agreement1. Moving on…

Stocks were volatile Friday, with a big puke as Russia Invasion warning headlines dropped and were taken seriously this time... Everything closed red today with Nasdaq the biggest loser, all closing near their lows.

That realization, considering US equity valuations have never been higher (combined with a collapse in US consumer confidence) have many wondering just where (or if) these two lines will ever converge.

Remember the K Shaped Recovery? It is real.

Then around lunchtime today, a series of reports of an imminent Russian invasion sparked turmoil in all markets. We put out a courtesy note to members since this kind of qualified as global geo-political risk. Here’s an excerpt.

1-PBS makes statement that invasion of Ukraine by Russia imminent

2-stocks drop, oil ramps, gold rallies, dollar rallies, Bonds drop confirming fears if not reality

3-WH denies, then says "not yet" but worried

4-Everything backs off a little

5-Media starts doubling down on "invasion by Tuesday"

6-Markets reassert their war-fear behavior- Gold, Oil up, stocks down, Bonds were well off of their lows as flight-to-safety and rate hike chances greatly retreat

The full note is unlocked here

And from that moment on, hell broke out with Europe closed.

Sectors

Consumer defensives, Energy, Basic materials did well

Longer duration tech and some utilities did poorly

Aerospace did well?

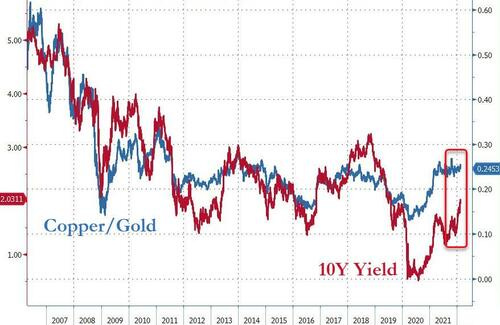

BUY THE WAY: COMMODITIES AND BONDS

If Dr.Copper (relative to Gold) is right, then 10Y yields have around 100bps further to go at least.

If it is wrong, adn the lines converge then Copper will fall relative to Gold rather quickly. Either way convergence impies stagflation or worse now.

These two lines converge when any of these three things happen. Gold rallies, and/or Copper drops, and/or Bond rates go up. it is a very trusted indicator for bond folks tracking recession/inflation risk.

Commodities

see charts section for graphics

Oil prices exploded higher on the Russia headlines with WTI topping $94.50 for the first time since Sept 2014.

The dollar ended the week marginally higher.

Cryptos were mixed this week with Ethereum tumbling back to unchanged on the week, Ripple outperforming and Bitcoin managing modest gains

The Ruble was routed today- a sign that this is not good for Russia either

Bonds

The Russia headlines sent rate-hike expectations lower for March.

massive bear flattening in the curve, actually inverting

Treasury yields soared this week as the short-end exploded 27bps - most since Volcker (on a sigma basis)

But then 'Russia Invades' reports sent yields plunging

And the swaps market is now pricing for a rate-cut at some point next year - i.e. Fed policy error

GoldFix Friday WatchList:

Complete Watchlist Here

Crypto Weekend:

2. Technical Analysis

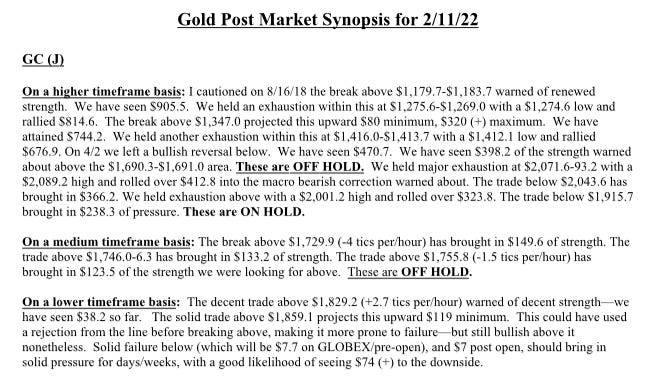

Report Excerpts Courtesy MoorAnalytics.com

GoldFix Note: Do not attempt to use price levels without symbol explanations or out of context. Moor sends 2 reports daily on each commodity he covers. The attached are non-actionable summaries.

Gold

TECHNICALLY BASED MARKET ANALYSIS AND ACTIONABLE TRADING SUGGESTIONS Moor Analytics produces technically based market analysis and actionable trading suggestions. These are sent to clients twice daily, pre-open and post close, and range from intra-day to multi-week trading suggestions. www.mooranalytics.com

Bitcoin

Energy

Go to MoorAnalytics.com for 2 weeks Gold, Oil, and Bitcoin reports free

3. GoldFix and Bitcoin Podcasts

Almost Like Covid Didn’t Happen…

Gold behavior is changing…

Bitcoin is tied to US Data… Take advantage of that when you can…

4. Charts

Dollar Index

Bond Yields

Gold

Silver

Crude Oil

Copper

Bitcoin Futures

Charts by GoldFix using TradingView.com

5. Calendar

Some of the upcoming week’s key data releases and market events.

MONDAY, FEB. 14

8:30 am St. Louis Fed President James Bullard interviewed

TUESDAY, FEB. 15

8:30 am Producer price index Jan. 0.5% 0.2%

8:30 am Empire state manufacturing index Feb. 10 -0.7

WEDNESDAY, FEB. 16

8:30 am Retail sales Jan. 2.0% -1.9%

8:30 am Retail sales excluding autos Jan. 0.8% -2.3%

8:30 am Import price index Jan. 1.4% -0.2%

9:15 am Industrial production Jan. 0.4% -0.1%

9:15 am Capacity utilization Jan. 76.7% 76.5%

10 am Business inventories Dec. 2.1% 1.3% 10 am NAHB home builders' index Feb. 83 83

2:30 pm FOMC minutes

THURSDAY, FEB. 17

8:30 am Initial jobless claims Feb. 12 222,000 223,000

8:30 am Continuing jobless claims Feb. 5 -- 1.61 million

8:30 am Building permits (SAAR) Jan. 1.74 million 1.89 million

8:30 am Housing starts (SAAR) Jan. 1.70 million 1.70 million

8:30 am Philadelphia Fed manufacturing index Feb. 19.7 23.2

11 am St. Louis Fed President James Bullard speaks

5 pm Cleveland Fed President Loretta Mester speaks

FRIDAY, FEB. 18

All day Chicago Booth School-New York Fed meetings

10 am Existing home sales (SAAR) Jan. 6.10 million 6.18 million

10 am Leading economic indicators Jan. 0.2% 0.8%

10:15 am Fed Gov. Christopher Waller speaks

Main Source: MarketWatch

Zen Moments:

Monkey Reacts to stuffed monkey:

Disclaimer: Nobody is telling you to do anything here. Anybody who tells you to do something without first intimately knowing your personal situation is irresponsible at best and manipulative at worst. Worse, anyone who acts on other people’s opinions without first doing an inventory of their own situation shouldn’t be surprised if they lose money.

6. Premium: Precious/Feature Analysis

Below the fold: Jobs, CPI, Ukraine and Gold

7. Premium: Research Reports

Below the fold- GS on Commodites, BBG on Backwardation, and Stocks that benefit from positive Interest rates

The real economy can’t run on financial assets excerpt:

The opportunity to buy commodities has rarely been better, Near-record roll yields drive up investors total return, Commodity supply is less nimble than money supply, and Physical markets are dislocating from financial markets

Self-Promtional Note: For $5 a month our paid subscribers get more in one of these reports (without ads) than from a month of legacy media clickbait nonsense or youtube hyperbole. For $150 a year subscribers get access to doctorate level economic/market lectures. Seems kind of cheap.

People who want analysis and tools to better map their own finances including traders, retirees, and students are starting to see the value here. And we’re grateful.

Have a great week. - GoldFix