Weekly: Warning- Russian Gold For Sale

Bulls Should Want Low inflation for the Moment

Housekeeping: This Monday and every Monday we do a Silver/Gold podcast on Arcadia Economics. We request you take a look and subscribe to the other excellent silver-based content on that site. Much of the content in our podcasts builds on comments we make here on metals.

SECTIONS

Market Summary— Russian Fallout may be beginning

Research— GF, JPM, GS, TD, BOA

Week’s Analysis/Podcasts— China Gold, BRICS Oil, US CHiPs

Charts— Metals, Energy, Forex

Calendar— Powell speaks, Unemployment

Technicals— GC, CL, BTC, SPX

Zen Moment— All Gold is from space, Panda

Full Analysis— GF, JPM, GS, TD, BOA

1. Market Summary

The Dow ended a 4-week losing streak, breaking back above its 100DMA

The S&P tested its 200DMA then ripped back higher, thru its 50DMA

The Nasdaq tested its 200DMA and then dip-buyers ran wild

Consumer Staples and Utes were the only sectors in the red for the week while Materials outperformed

Goldman noted that net flows into global equity funds remained negative in the week ending March 1 (-$7bn vs -$7bn in the previous week), driven by outflows from US equity funds, which have remained negative for four consecutive weeks. Flows into global fixed income funds accelerated (+$8bn vs +$5bn in the previous week) on stronger inflows into government bond funds and IG credit, which had seen more mixed flows in recent weeks... and who can blame them for rotating...

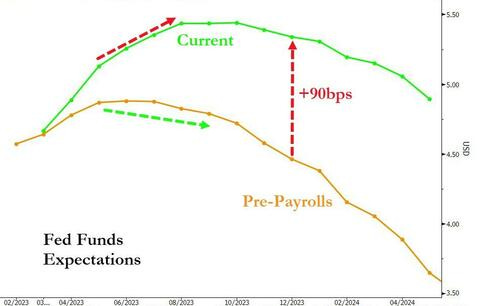

We would note something ZH posited and add a perspective to it. They note along with the accompanying graph:

For some context as to how massively the market has shifted its perception about The Fed's rate trajectory, here is the before and after picture of the short-term rate curve since February's blowout payrolls print...

This gives a very real clue as to how much the Fed fund expectations could revert back if the February payrolls (due next Friday) contradict the January payrolls.

Basically: Wall Street was taken aback by the explosive Payrolls last month and never recovered.What happens to this curve if the Jan Payrolls were an aberration? What happens to stocks? If the January payrolls were undone, it could show significant upside in stocks.

This is not a prediction, merely a measure of the upside if next week’s payrolls are disappointing. For context, we note this past week was the first one in a while in which the market rallied on weak economic data and largely ignored strong inflationary data.

Sector/Technicals

Tech and basic materials both did well, not typical of the last few weeks

Energy Explorers outperformed,

Healthcare is now on a yo-yo week to week

Commodities

Gold surged over 2% this week back above $1850

Inflation expectations (swaps) have surged back up near cycle highs.

Oil prices plunged early on after WSJ report of a rift between Saudi and UAE - that was denied within an hour and WTI exploded higher, tagging $79

Bonds:

Treasury yields were lower in longer term bonds

This is the ideal behavior for those hoping for a soft landing and the first time we’ve seen it in a while

Crypto:

Crypto got destroyed even with stocks up. And it happened all in 30 minutes Thursday

Bitcoin trended sideways all week between $23k and $24k until last night in Asia when it puked back to $22k (potentially after all the headlines around Signature Bank), breaking below the 50DMA ($22870) for the first time since Jan4th

2. Research Excerpts:

Themes: No Gold research and very little to no Oil research right now but we found something very interesting regarding Russian behavior… Banks are weighing January inflationary spikes as now a one-off in light of the data last week. Goldman recaps the Friday Trading day and more.

1- Gold: JPM Confirms Russia Sold Gold in January, and Bulls Should Want Low Inflation Right Now

Having thrown in the towel on any good Gold research this week, we started looking into Oil. And there we saw the reason for no Gold recommendations. It also confirmed Goldman’s tepid Can the Gold Comeback Continue? as well as the recent selloff Gold weathered. Russia is now a seller.

The big risk for a major move lower in Gold is now a product of Russian financial risk. Here is why.

CONTINUES AT BOTTOM…

2- Wells Fargo: Maximum Employment but Not Much Price Stability

The key thing to understand from today's ISM services report is that activity is not slowing much and that is keeping pressure on prices and on margins. The resilience of service sector activity may turn up the pressure on policymakers at the Federal Reserve to do more to combat inflation

The fact that this is occurring alongside an upswing in hiring gives the Fed the green light for further rate increases. Most forecasters, ourselves included, expected services activity to cool somewhat in February, but the 55.1 reading for the headline figure was not nearly as much of a slowing as expected.

CONTINUES AT BOTTOM…

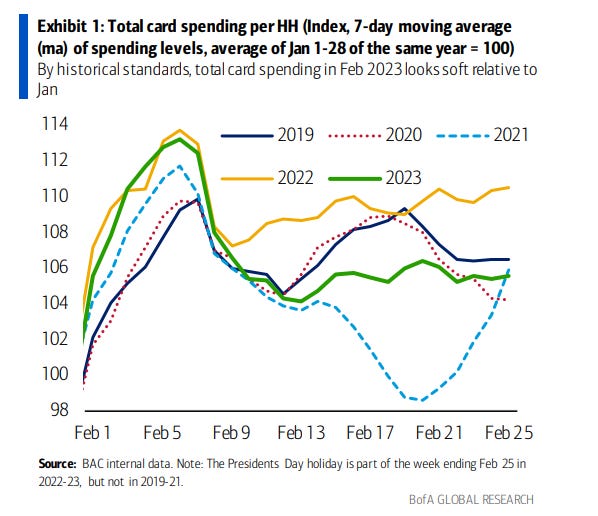

3- BOA: Is inflation Re-accelerating or contained- Credit card analysis

The big question A critical issue in terms of the US economic outlook is how long the acceleration in activity that started in January will continue. Here we use BAC aggregated credit and debit card data through February 25 to attempt to answer this question.

The concern, however, was that there might have been a lot of “one-off” spending in January. Some consumers might have made big-ticket purchases or dined out to “celebrate” the increase in their income. Post-holiday clearance sales and unseasonably warm weather in January would have further incentivized such activity.

CONTINUES AT BOTTOM…

4- Goldman’s Friday Post Close Recap

Desk activity, Flows, Europe, CTAs, Oil, and more

Above: World Interest Rate Probability (WIRP) measure uses fed funds futures to infer the implied probability of future FOMC decisions.

CONTINUES AT BOTTOM…

5- Hedge Fund Sector Performance

MUCH MORE AT BOTTOM…

3. Week’s Analysis/Podcasts:

CHIPS are a Tool of Economic War Against Russia and China- ZeroHedge version

China's Central Bank Likely Owns 4,309 Tonnes Of Gold, More Than Double What Is Officially Disclosed

Energy: The US Has Declared War on Brics Oil- ZeroHedge version

New John Paulson Interview Transcribed- ZeroHedge version

4. Charts:

Metals

Energy

Forex

5. Calendar

MONDAY, MARCH 6

10.00 am Factory orders Jan. -1.8% 1.8%

TUESDAY, MARCH 7

10:00 am Fed Chairman Powell testifies to Senate

10:00 am Wholesale inventories Jan. -0.4% 0.1%

3:00 pm Consumer credit Jan. $25.0B $11.6B

WEDNESDAY, MARCH 8

8:15 am ADP employment Feb. 210,000 106,000

8:30 am U.S. trade balance Jan. -$68.7B -$67.4B

10:00 am Fed Chairman Powell testifies to House

10:00 am Job openings (JOLTS) Jan. -- 11 million

2:00 pm Beige Book

THURSDAY, MARCH 9

8:30 am Jobless claims March 3 193,000 190,000

10:00 am Fed Gov Waller speaks

FRIDAY, MARCH 10

8:30 am Employment report Feb. 225,000 517,000

8:30 am U.S. unemployment rate Feb. 3.4% 3.4%

2:00 pm Federal budget Feb. -- -$217B

Main Source: MarketWatch