Gold as Proxy: Where is gold headed and what does it mean for my 401k?

If an equity friend asks about gold in context...give them this

Share this with a favorite non-believer relative please.

Gold Repatriation, Market Rotation, and Basel III: A Structural Shift

Introduction

The financial markets are undergoing a noticeable shift, driven by macroeconomic factors, capital rotation, and policy changes. The ongoing discussion about gold repatriation and its impact on GDP, combined with Basel III regulatory requirements, underscores the evolving nature of global financial positioning. This short essay will explore recent market trends, the implications of gold’s role in trade and monetary policy, and the regulatory landscape ahead.

The following current events will be touched upon in context of Trump’s first two months:

Gold repatriation as indication of world-view shift

Germany’s increased deficit spending

Tariffs

Gold’s hidden effect on GDP

Fed policy and the USD

Rotation from Equities to Commodities

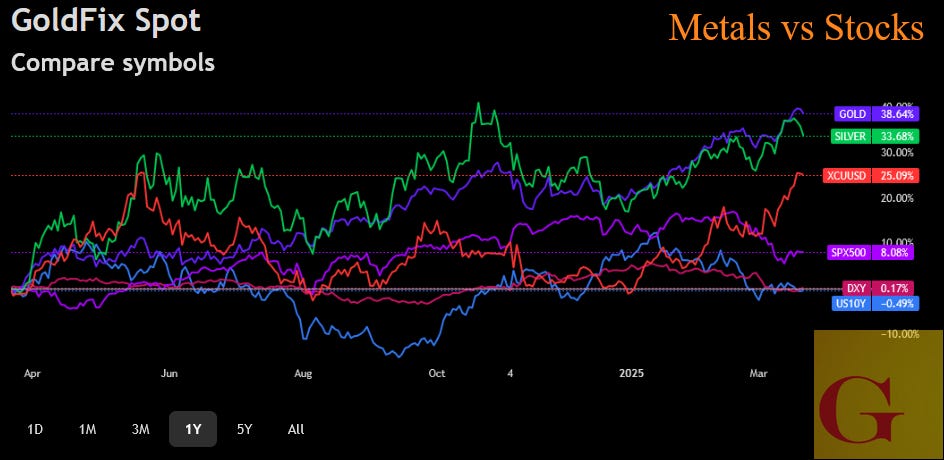

A key market trend emerging is the rotation from equities into hard assets. Gold, silver, and copper are outperforming stocks, a reversal from previous risk-on market conditions. The S&P 500 saw strength late last year, but equities have since backed off their highs. In contrast, gold has firmed up, suggesting capital is reallocating into safer, inflation-resistant assets. But its not just about inflation risk. it’s about a slight return to sanity.

This shift indicates a deeper movement of funds away from technology stocks and high-flying promissory stocks domestically, and also away from US stocks and into international ones globally. Both domestic flows and the rotation out of US is a rebalancing of investments to better reflect global economic potential with a horizon of about 4 years.

In this way, institutional investors (like pensions and firms like Blackrock), and banks are positioning ahead of anticipated changes. A typical result would be:

Take profits in Tech, buy dividend stocks

Sell US companies, buy foreign companies

Specifically this time it is:

Sell Tech, buy dividend stocks, buy bonds, buy some gold, buy some mining stocks- this last part is very new

Sell US, buy EU, China, and Japan equities- for different economic reasons, but for one unified reason— Given the global monetary changes in play, they will benefit.

Rebalancing happens all the time with these types, but this time it is aligning with secular changes discussed here many times involving gold, mercantilism (protectionism/tariffs), and a lessened dependence on the USD for global trade.

If you are old enough to remember what happened to global markets when the Berlin wall fell; This is not unlike the Berlin wall going up.

In this sense we believe these moves, while not necessarily explosive, are not temporary and will manifest in fits and starts. When this rebalancing is over, the new equilibrium levels between nations and amongst different asset classes will be permanently altered. The evidence to this is Gold, Silver, and Copper’s price changes over the last year as compared to stocks.

These rallies occurred during a decrease of inflationary pressures.

Metals garnered hardly any headlines, yet have outperformed everything the US has to offer. Further— Gold has retaken its status as a leading indicator of change beyond it’s inflation-hedge status. Gold predicts economic policy once again, as it did before the 1990s. Which brings us to the Dollar.

The Role of Currency and Global Capital Flows in Stock

The weakening U.S. dollar further supports this. While the exact mechanism driving the dollar’s decline remains unclear, one possible explanation is market anticipation of future interest rate cuts. A weaker dollar aligns with broader macroeconomic expectations that rates will need to be lowered at some point to stem the stock market outflow by lessening opportunity cost. That’s the macro rationale, yet it’s not even half the story this time. Secular changes are driving this bus.

The USD actually needs to decrease versus other currencies to facilitate the changes mentioned up top. The world is slowly dedollarizing as trade increasingly is conducted in local ( more Gold-dependent) currencies. Less long term holders of USD ( to buy oil for example) means lower USD value. Current USD weakness is not just about anticipating Fed policy used to prop up stocks this time. It’s about things outside US control.

Internationally, currency dynamics play a role. Right now, the euro is strengthening as Europe drives some global equity market flows. Germany has raised its spending cap to allocate more funds toward infrastructure and defense. This has led to a repatriation of capital into euros, as investors shift allocations from U.S. assets to European equities.

Germany's new financial positioning echoes previous periods of capital realignment. Some parallels exist with the post-Cold War era when German infrastructure spending created a realignment of global capital flows. Today, European monetary policy and increased fiscal activity are altering the structure of international investment. This is all in response to Trump’s Tariffs and the US anticipated withdraw from providing the bulk of European military protection under NATO.

Global disclocations are inevitable during events like these; Hence the rise in Gold as a touchstone of safety and globally recognized tool of trade in an increasingly mistrusting world.

Gold Repatriation and Its Impact on US GDP

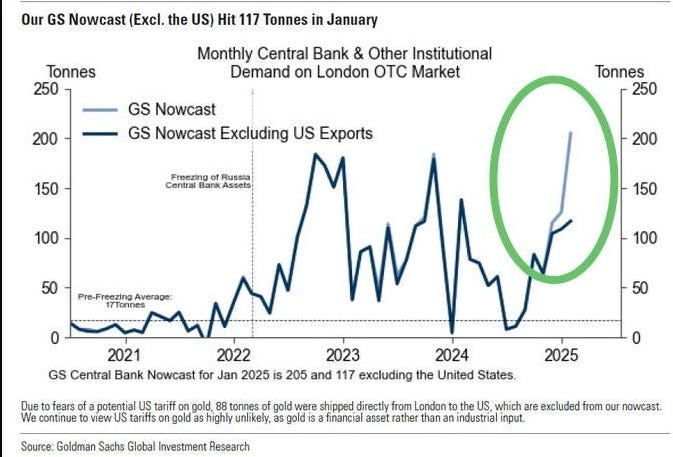

One of the more recent discussions revolves around the implications of gold repatriation. Large-scale gold imports into the U.S. have widened the trade deficit. However, because non-monetary gold is excluded from GDP calculations, these transactions do not contribute positively to economic output.

Goldman Sachs has addressed this issue twice, emphasizing that rising gold imports are expanding the trade deficit but not benefiting GDP. The exclusion of gold from economic output stems from its classification as a non-productive asset under traditional economic frameworks.

JP Morgan has also highlighted this effect, referencing gold imports as a factor reducing first-quarter GDP estimates to 1%. Their analysis incorporates Bureau of Economic Analysis (BEA) trade data, which categorizes imported gold as “non-monetary” unless refined into standard 400-ounce bars. The classification loophole impacts how gold transactions are reflected in economic reports.

The distinction between monetary and non-monetary gold introduces another layer of complexity. We aim to now simplify.

If gold enters the country in a non-standard form, it does not count toward GDP. However, once refined and classified as monetary, it becomes part of financial reserves, changing its economic treatment. All that gold (2,000 tonnes) will be refined, after which it will be suitable for something economic even by their own biased data standards. Essentially, All Gold is Monetary Gold

Why Is the U.S. Repatriating Gold?

The growing volume of repatriated gold raises fundamental questions about U.S. monetary positioning. Theories regarding the purpose of these transactions include:

Covering Bullion Bank IOUs – Bullion banks that previously leveraged gold reserves through derivatives and rehypothecation may now be required to reconcile outstanding obligations.

Basel III Compliance – New regulatory requirements demand banks adjust their balance sheets, particularly regarding tier-one capital.

Preparing for a New Financial Instrument – Potential uses for repatriated gold include gold-backed bonds, stablecoin initiatives, or sovereign wealth fund allocations.

Each of these potential explanations suggests a strategic realignment rather than a short-term arbitrage move. It also is consistent with and predicts the future bias of capital flows under a more protectionist, less cooperatively global economic backdrop mentioned in the introduction.

Basel III and Coming U.S. Banking System Adjustments

The implementation of Basel III in the U.S. on July 1, 2025, adds another layer of urgency to gold repatriation. The regulatory framework, which began in 2009 but has been repeatedly delayed, will require U.S. banks to classify gold as a tier-one asset.

Historically, Basel III was designed to stabilize the banking system by ensuring financial institutions hold sufficient high-quality liquid assets. The gold reclassification within Basel III’s framework means banks can use physical gold as collateral at full value rather than at a discount.

European banks have already transitioned to Basel III standards, but U.S. banks are now required to comply. (Important footnote on why the EU leads on this1) This shift may explain why gold is being relocated ahead of the implementation deadline.

Potential Monetary Policy Shifts

The repatriation of gold also aligns with broader monetary shifts. The potential monetization of gold—whether through sovereign wealth funds, collateralized bonds, or other financial instruments—reflects a strategic repositioning.

Gold-backed financial products would represent a shift in U.S. monetary strategy. While central banks have traditionally downplayed gold’s role in the financial system, the increased accumulation suggests that institutions are acknowledging its importance.

Conclusion: Structural Shifts in Markets and Policy Well Beyond the Norm

The financial markets are undergoing a transition, with capital shifting from equities into commodities, particularly gold. The weakening dollar and European monetary policy adjustments are influencing global flows. At the same time, large-scale US gold repatriation is happening in spite of their pronounced negative impacts to GDP calculations and trade balance metrics.

The motivations behind U.S. gold repatriation remain open-ended but align with regulatory, monetary, and strategic objectives. Basel III implementation, the restructuring of tier-one capital, and potential future gold-backed instruments all suggest a major shift in financial positioning.

Gold’s role in global markets appears to be evolving from a sidelined reserve asset to an active component of financial stability and economic strategy. The ongoing developments in gold repatriation, Basel III compliance, and capital flow realignments will define the next phase of monetary policy adjustments.

These serve as indicators of current stock valuation changes.

understand this perceived EU/US pecking order is a formality. The US DRAWS UP global banking rules. The EU implements them first as a field test. THEN the US adopts them. All monetary rules are US in origin

Wow reading this is just like a photo..you instantly see the big picture... Well said Vince. Thank you!

Thanks Vince. Why didnt they repatriate all that gold at $1650, when Basel III came into effect for everybody else? Doesnt make sense to be doing it now at $2800-$3000. Whats the thinking behind preferring to pay well over $1000 an ounce for it?