Gold and Silver are pivoting from being an inflation hedge to being a bank solvency hedge with almost no disinflationary pause in the middle. The disinflationary sweet spot (aka Goldilocks) between Inflation and Deflation is almost impossible to find for the Fed .This is how Anti-Goldilocks manifests

SECTIONS

Market Summary— Very bipolar markets

Week’s Analysis/Podcasts— Gold, SVB, and Baseball

Research— Gold, Silver, PGMs, Banks, Hartnett and more

Charts— Metals, Energy, FX, Bonds

Calendar— FOMC

Technicals— GC, CL, BTC, SPX

Zen Moment— Star Fish lite

Full Analysis— ANZ, BOA and MS

1. Market Summary

A mixed picture for stocks on the week withe Nasdaq the big outperformer while Small Caps were weakest. The Dow ended the week in red and the S&P slipped lower Friday but ended green...

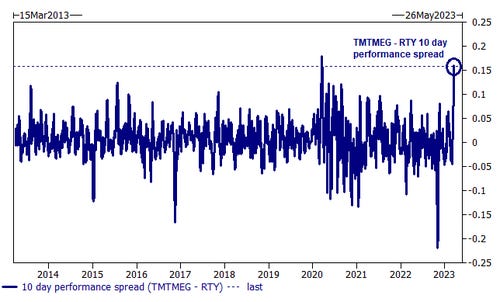

That huge outperformance of mega-cap tech over small caps is practically unprecedented. As Goldman notes,

over the last 10 sessions, the gs basket of mega cap tech stocks is up 6.2%

over the last 10 sessions, the russell 2000 is down 9.8%

this 16% spread is the second highest of all time (one data point in Mar2020)...

There has been a clear shift to tech stocks, and an even more clear shift to the ultra high market capitalization names

Gold & Silver:

It is just amazing that with this much grass roots interest not just in physical metals, but in GLD and SLV from first inflation and now banking fears that no major bank is covering Gold closely.

Sorry did we say amazing? We meant obvious… as in obvious you don’t talk about what you fear, especially when every time it upticks your own industry’s existential angst gets exponentially bigger.

Anyway.. we used to read ANZ reports a while ago, and got lucky and saw one yesterday. These guys give the metals some professional respect ( bullish, not cheerleaders) and we will be personally reaching out to them for more next week.

It is a must read for Silver and Gold people whether physical, futures, retail or professional.. Coins, Bars or ETFs. More in Section 3 below

Sector/Technicals

Gold miners, Tech screamed higher.

The S&P was unable to hold above its 200DMA

Banks destroyed, exchanges did well, Energy killed

Office REITS were crushed this week

VIX has broken up into a new higher-vol regime for now

European bank stocks collapsed,First Republic Bank tumbled back down to recent lows, despite billions in handouts from the big banks

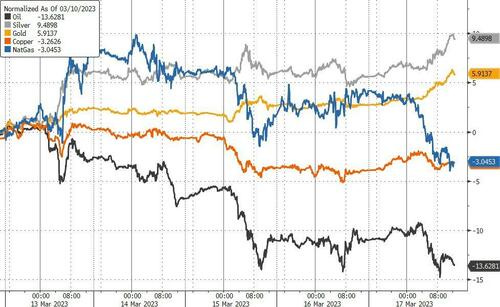

Commodities:

Gold soared this week, back above $1950, to its highest since April 2022

Silver outperformed Gold on the week

Crude, copper, and NatGas swooned

WTI puked to a $65 handle - its lowest since Jan 2022

The dollar ended the week lower, after a roller-coaster midweek

Bonds:

2 years destroyed shorts on the week again

Treasury yields were lower on the week with the short-end massively outperforming

The last 7 days in 2Y UST yields ( close-to-close) have been unbelievable (and ended below 4.00%): -20bps, -28bps, -61bps, +27bps, -36bps, +27bps, and -30bps

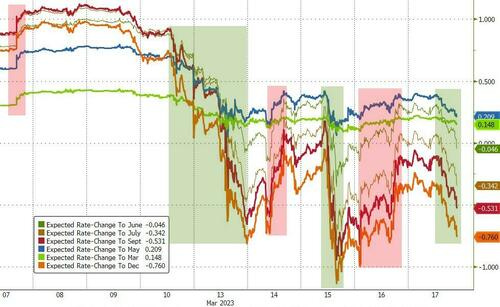

Fed Rate hike expectations whipped all week

Imagine the biggest bond market in the world trading like DogeCoin

The inversion backed off (“resteepening”) mightily implying that the recession is in full bloom and markets demand a lower rate to fight it off.

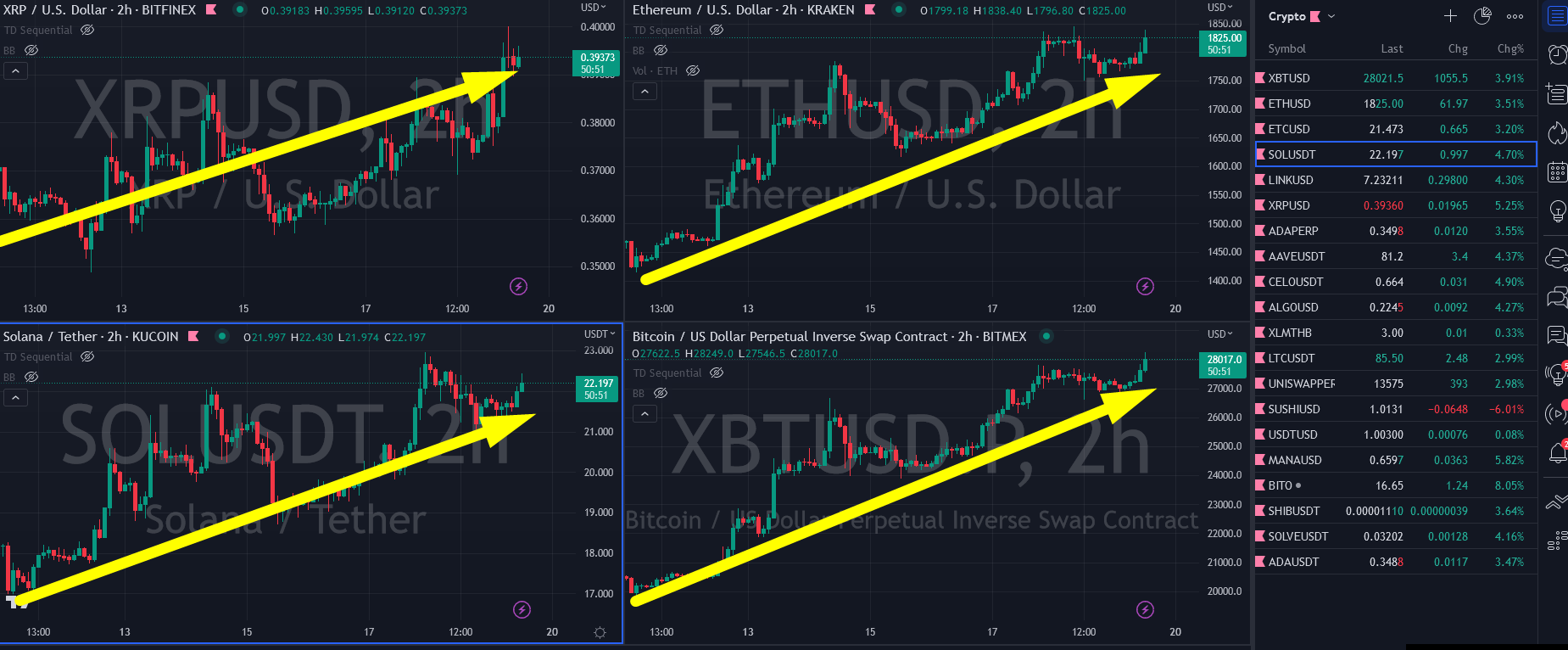

Crypto:

Crypto had a big week as either QE or bank insolvency (or both) is back on the table with Bitcoin dramatically outperforming.

Bitcoin topped $27,000 Friday for the first time since June 2022

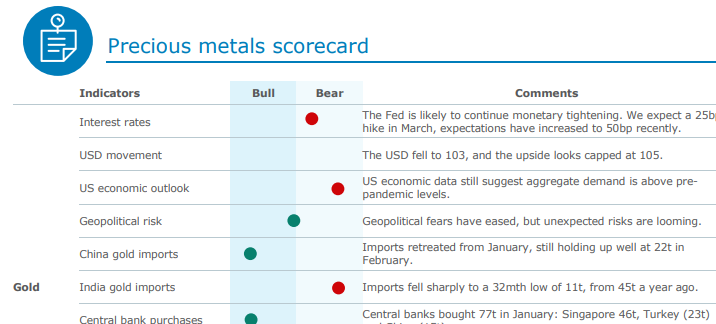

Very nice report by ANZ on Gold, Silver with a thorough “scorecard” for every precious metal. We hope to see more from them this way.

Here are some excerpts from the excellent 16 page report:

Gold prices will follow the shifting market expectations of the Fed’s terminal rate. A repricing above 5.5% could be a downside risk in the short term, but it will not be a game changer.

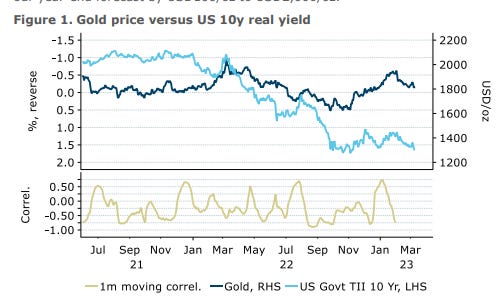

Conventional gold’s driver coming into play Gold’s negative relationship with real rates has been weakening over the past few years. The historical sensitivity has fallen from 13% for every 100bp increase in US 10y real yields to 3% and 1% since 2018 and 2020, respectively.

In 2022, the 10y real yield rose by 260bp, while gold was largely unchanged. Negative macro factors of rising yield were offset by strong purchases by the central banks and physical demand last year

Precious Metals Scorecard excerpt:

Price Action:

Includes some professional assessments on the following :

Short-term volatility, but upside bias remains intact