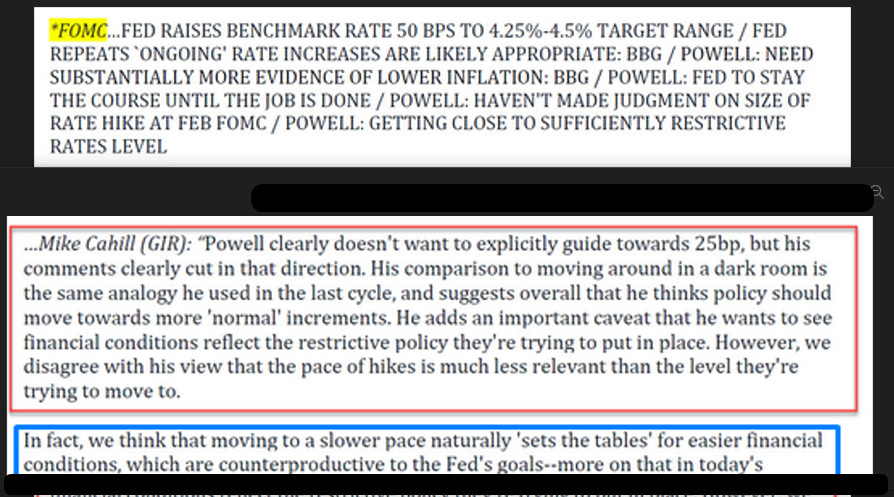

Weekly: Powell admits "moving around in the dark" again

Two Inflationary Paths, No Destination

They Fed has settled on a preferred path to the terminal rate of 25bps per hike. But they do not know the terminal rate. They picked the slowest path because they do not know where they are going anymore.

Housekeeping: Happy Hanukah and Merry Christmas to all this holiday season.

SECTIONS

Market Summary— Two paths, no destination

Research— BOA, JPM, TD

Week’s Analysis/Podcasts— Frogs, Fed, Finance

Charts— Metals, Energy, Forex, Bonds, Crypto

Calendar— PCE Friday

Technicals— Special Gold comment

Zen Moment— Letting go

Full Analysis— Oil, Copper, Macro, Charts

1. Market Summary

Stocks dropped for a second straight week with Nasdaq the biggest loser this week. Ugly US macro data and hawkish inflation speak were the culprits this time. Here are some choice quotes (our comments in lower case)

DALY: "INFLATION IS TOXIC", FED "IS FAR AWAY" FROM ITS PRICE-STABILITY GOAL, MAY NEED MID-4% OR MORE JOBLESS RATE FOR LABOR-MKT BALANCE- they want unemployment higher

FED HAS `MORE WORK TO DO ON INFLATION,' IT'S TOO HIGH- now they tell us

DALY: DON'T KNOW WHY MARKETS ARE SO OPTIMISTIC ON INFLATION- mkts aren't optimistic on inflation. They are trained by you to expect to be bailed out

MESTER: HAVEN'T SEEN IMPROVEMENT ON SERVICE-PRICE INFLATION- which is entirely the opposite of what you said would happen. You thought goods inflation would stay firm and you could get services inflation down—you were wrong once again

One thing we have learned and shared with readers since this cycle started is we believe the entire country has been spoiled by the Fed bailout put since 2009. And because of this; “hope” will spring eternal every chance it gets. It can manifest in dead-cat bounces for sure.

On the Path to Ineffectiveness

The reason we bring it up today is because the Fed is likely focused on the markets’ interest rate path expectations of inevitable easing again. The market is once again believing the Fed will ease sooner rather than later.

Like previous rallies, the Fed will continue driving its message to undo the decade of dovish expectations it trained us all to wait on. But easing is not coming until we get more confirmation of inflation easing to relax them. That, or if something actually breaks.

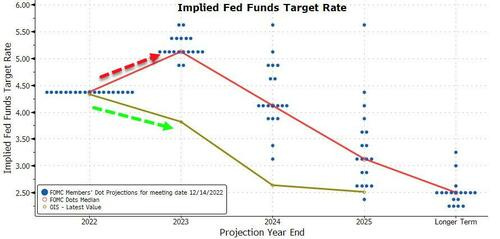

Further to that, The FOMC meeting showed us the Fed is genuinely not sure when the rate hikes end. Their focus on getting hikes down to 25bps per shot is coupled with a dot plot drifting even higher over time. We elaborated on this in our “boiled frogs” post.

In a nutshell: They have settled on a path to the terminal rate. But they do not know the terminal rate.

The Fed has settled on a preferred path to the terminal rate of 25bps per hike. But they do not know where or when it ends. They picked the slowest path because they do not know where they are going anymore. Five, six, and seven percent are all on the table. The 25bp tactic is a function of fear of breaking something while still claiming to fight entrenching inflation. ChatGPT can do this just as well.

They should be stopping hikes now because of the trend in data, but cannot because of the data itself coming down form a too high plateau. So they are trickling rate hikes now. It is unenviable trying to manage long-term baked in crash risk (from a decade of loose money) while trying to make sure long term inflation doesn’t re-entrench.

The FOMC is trying to look like they know where they are going, but they do not. Powell knows how the Fed is going, but not where. They hope data can give them a clue soon and are thus moving to raise rates more gingerly. We understand that and don’t disagree. But they did this by accepting praise and taking credit for prosperity they had little to no contribution to. Worse, they repealed market cycles at a time when they would have been healthy for years.

BUT: the problem isn’t the approach, it is the impression they give being in control by showing a regular path of 25bps coming soon. When in reality, they are picking the lowest level to use because they don’t know where it ends. They are kicking the decision-can down the road once again.

Here is how one Goldman trader put it:

"Powell doesn't want to explicitly guide towards 25bp, but his comments clearly cut in that direction. His comparison to moving around in a dark room1 is the same analogy he used in the last cycle, and suggests he thinks policy should move towards more 'normal' increments"

h/t ZH

G-d help us if the markets figure this out before the data helps the Fed decide on a real path.

Finally- the movement to raise the inflation target to 3% or more is gaining momentum. The Fed is now buying time for either the inflation to drop, or the target to be raised.

Here are those moving parts combined:

The Fed needs good inflationary data to justify stopping hikes.

They are petrified the economy will collapse if a tipping point is reached well before better inflation data shows up.

They are actively being pressed to raise the inflation target, which even if they don’t want to do, they certainly will be guilt-free about if it happens.

Until 1, 2 and/or 3 happen, they will trickle rates higher for as long as it takes, with a terminal rate or date unknown.

Rates could easily top out at 6% if nothing breaks as they make teeny tiny rate hikes now. Frogs in a pot expecting it to stay hot much longer. Only the data bails them out now.

Inflation is definitely dropping by empirical measures. But it is not going away. Why? Because the Fed cannot kill it fast enough for fear of toppling markets too hard.

Yet by letting inflation fester longer, they are training people to expect it to be here for a much longer time. That will be self-fulfilling. Which is exactly what they say they don’t want to happen: having inflation expectations get entrenched in the psyche. More people will go on strike, and wage spirals explode. Game over.

Forgive the analogy but: you cannot come off a cocaine high with heroin while titrating with caffeine. It is not going to work without inflation basing much higher and/or unemployment growing to be over 5%

Inflation will most definitely rebalance at a higher level if they are successful. Inflation will explode if they are not successful. The economy will collapse if they are too aggressive.

Sector/Technicals

Meta is bucking trend as it would benefit most from a Tik-Tok ban

The S&P ramp at the close lifted it back to its 50DMA

Basic materials took cues from the Fed and ignored China reopening

Oil in part looked at the Biden admin announcement of refilling the SPR

Commodities:

Gold and silver ended the week flat to very slightly lower.

Gold futures bounced back up to $1800 rejecting the lower area again SEE THE NOTE IN TECHNICALS

Crude bounced higher after two ugly weeks, with WTI bouncing from a $70 handle up to almost $78 before fading back to $74 after The Fed.

The Dollar ended the week unchanged, recovering all of its post-CPI plunge on the hawkish Fed statement

Bonds:

Treasury yields were all lower on the week with the short-end outperforming (2Y -16bps, 30Y -3bps) on the week

Crypto:

Big round-trip in cryptos this week, running higher on the soft CPI and erasing gains on a hawkish Fed.

H/t Zerohedge for data and some graphics.

2. Research Excerpts:

BOA’s Flow Show- Founders see ZH prem for a write up on this. We can discuss Sunday.

Quicker labor markets break quicker end to bear market, start new Wall St bull market; we still say shadow banking credit event marks Big Low in ‘23

Global Metals- Copper focus. As goes copper, so goes Silver right now

BOA Macro- 2023 key themes

TD CTA Analysis- Silver CTAs are long now. Gold still short

JPM Oil- All about the SPR buyback

GS Chart pack- 2022 eye candy

CONTINUES AT BOTTOM…

3. Week’s Analysis/Podcasts:

JPM: "For countries that see CPI exceed 5%, it takes around 10 years for CPI to fall back to 2%.”- ZeroHedge version

Futures Curve Structure- Uni. Lecture

Oil Markets on Sick Leave as 2022 Comes to a Close- Brynne Kelly

Goldman's 2023 Supercycle Report Unpacked- ZeroHedge version

Is Inflation Dead? No.- ZeroHedge excl.

4. Charts:

Metals and DX

Metals/PGMs

Energy

Forex

5. Calendar

MONDAY, DEC. 19

10 am NAHB home builders' index Dec. -- 46.2

TUESDAY, DEC. 20

8:30 am Building permits (SAAR) Nov. -- 1.51 million

8:30 am Housing starts (SAAR) Nov. -- 1.43 million

WEDNESDAY, DEC. 21

8:30 am Current account deficit Q3 -- -$251 billion

10 am Consumer confidence index Dec. -- 100.2

10 am Existing home sales (SAAR) Nov. -- 4.43 million

THURSDAY, DEC. 22

8:30 am Initial jobless claims Dec. 17 -- N/A

8:30 am Continuing jobless claims Dec. 10 -- N/A

8:30 am Real gross domestic product revision (SAAR) Q3 -- 2.9%

8:30 am Real gross domestic income revision (SAAR) Q3 -- 0.3%

8:30 am Real final sales to domestic purchasers (SAAR) Q3 -- 0.9%

8:30 am Chicago Fed national activity index Nov. -- -0.05

10 am Index of leading economic indicators Nov. -- -0.8%

FRIDAY, DEC. 23

8:30 am PCE price index Nov. -- 0.3%

8:30 am Core PCE price index Nov. -- 0.2%

8:30 am PCE price index (year-on-year) Nov. -- 6.0%

8:30 am Core PCE price index (year-on-year) Nov. -- 5.0%

8:30 am Real disposable income (SAAR) Nov. -- 4.6%

8:30 am Real consumer spending (SAAR) Nov. -- 6.2%

8:30 am Durable goods orders Nov. -- 1.1%

8:30 am Core capital equipment orders Nov. -- 0.6%

10 am UMich consumer sentiment index (late) Dec. -- 59.1

10 am UMich 5-year inflation expectations (late) Dec. -- 3.0%

10 am New home sales (SAAR) Nov. -- 632,000

Main Source: MarketWatch